You don’t need complicated, you need easy. You need step by step instructions on how to start a budget that will actually work for you. Done. Grab a seat, a coffee, and a notebook… we have work to do.

Update: 4/5/20 I know how stressful finances are right now with stay at home orders and the pandemic. I also know that I’m uniquely qualified to help you. I’ve helped hundreds of thousands of people get out of the paycheck to paycheck cycle (after trying and failing for years), by teaching them how to work with their unique personality to actually stick to a budget.

I’m giving you access to the insanely popular 90 Day Budget Bootcamp for FREE. Because I know that this program will change every aspect of your life. Take a look around. Because this is the LAST DAY you will ever sit around worrying about money. Let’s get to work.

Join the 90-day Budget Bootcamp for FREE here…

Unless you have a healthy cushion in the bank account, it’s not only important to start a budget, it’s important to know when money is going in and coming out. If you skip this step, then you run the risk of overdraft (when you spend more than you have in your bank account and get charged a fee).

This simple way of budgeting solves all of those problems.

There are a million different ways to track your budget, but for right now I want you to be able to do it on paper. This is important. Just trust me on this one. One or two months on paper, and then you can use any online tool or app you want. Stick with me.

One or two months on paper, and then you can use any online tool or app you want. But start on paper.

If you need extensive help on creating and sticking to a budget, the best resource I can give you is the free step-by-step class 90 Day Budget Bootcamp that walks you through not only how to create a budget, but how to set up the basic routines in your life that will support your efforts to save money. Because transforming your finances is about more than just the budget. This was the best thing that ever happened to us.

You can sign up for the 90 Day Budget Boot Camp class for free by clicking here or entering your email in the box below.

How to Start a Budget: Step by Step.

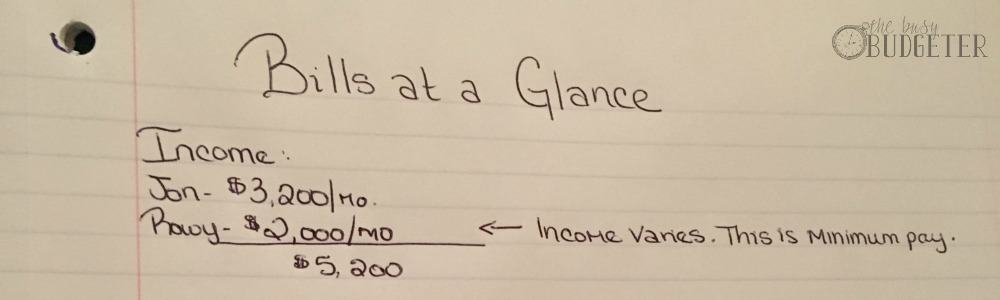

Step 1: Determine your monthly income.

For some, this is easy- they have consistent paychecks and no additional overtime. They can just add up their paychecks in a month. If you have irregular income, this is enough to create headaches on its own.

If you have irregular income then write down your minimum amount of income this month. This is the amount that you’re very sure you will be making this month.

Example: If you work from home doing data entry and you make anywhere from $1,000- $2,500 every month. Write down $1,000.

If you’re looking for ways to increase you income, you can find the 4 ways I make over $3,000/month as a stay at home mom here as well as a long list of the successful side hustles that will boost your income here.

We’ll deal with your extra income in a few minutes.

Step 2: Create a Monthly Budget Outline.

Grab a sheet of paper. Label the top of it with the month and year. On the top of the paper, list the income you just wrote down.

I call that dependable family income. You may make more than that in overtime or more sales, but that’s the amount you feel comfortable relying on.

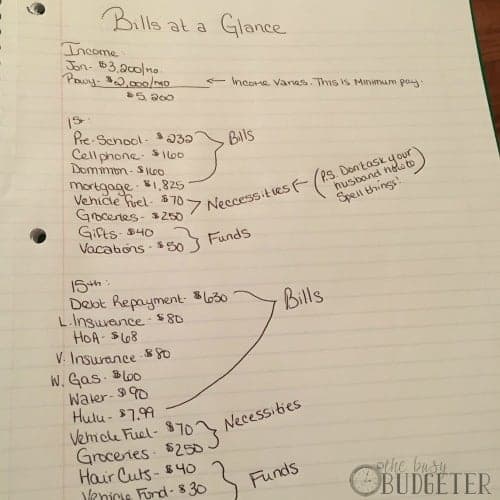

Now write down your pay dates. I’ll walk you through this using an example of being paid twice a month on the 1st and 15th. List those pay dates on the paper like this:

Start to list every bill you have, no matter how small. Separate them by when they are due and list the name and amount due under the 1st or the 15th on your paper.

Step 3: Set a Grocery Budget.

Now decide on a reasonable amount to set aside for groceries. If you’ve never tried to limit your grocery spending, aim high for now and reduce it later. The worst thing you can do is budget one hundred dollars a week, spend three hundred a week then give up.

If you need a basic idea, you can do 15-minute convenience meals at home and spend no more than $120.00 per week, including lunches for two adults (We could feed a small child on that same budget). You can see the menu plan for that here.

Total your groceries and your bills and subtract that total from your total dependable income. Don’t panic if you don’t have a lot of extra money to work with- we’ll work on that next week. This week, just write the numbers down and have an idea where you are now.

What if I have absolutely no idea how much to set aside for groceries?

If you typically use a debit/credit card for all of your purchases- go through the last 30 days of spending in your online bank account and add up the amount for every food-related purchase you made (include eating out).

If it was over $1,000 then shave off 20% and write that number down as your next month’s grocery budget. If that amount is still more than you can afford, you can attempt to shave it down more. However, I would caution that it’s incredibly hard to create lasting change with drastic cuts.

If you’ve been spending $1,600 a month and eating out several times a week, it’s going to be really hard to suddenly go to $500/month because spending $500 a month in groceries involves a ton of new routines. I want to transform your entire life over time. Not drastically cut your spending in a month and then have you relapse into exactly where you are now or worse. Always go for baby steps if you want a change to last.

I want to transform your entire life over time. Not drastically cut your spending in a month and then have you relapse into exactly where you are now or worse. Always go for baby steps if you want a change to last.

Hint: We had the most luck reducing our spending by going through The Grocery Budget Makeover. It’s only available twice a year though. Your best bet is to can get on the waiting list here.

Step 4: Substitute, Substitute, Substitute!

Are there any exchanges you can make that would reduce your bill amounts right now? Look for things that are cheaper but are the same or better than what you’re using right now. Here are a few of the most popular examples…

Exchanging Hulu or Netflix for cable.

Straight Talk or Ting for an expensive cell phone plan. (Hint: T-mobile seems to be offering competitive rates as well).

Using the library instead of buying books.

You can read about how we made $23,000 worth of substitutions here.

Choose one bill you can reduce and do it. Call and negotiate a new rate, or make a substitution. Reduce it and then change your list to reflect the new amount.

Your goal in the next few weeks is to continue making substitutions, but leave it at that for right now.

Step 5: Create Funds.

There are quite a few purchases that only need to be made infrequently, like Christmas gifts or vacation. The best way to handle these purchases by creating funds. List these purchases down and set a realistic frequency for which they need to be purchased. Here are a few examples from our funds list:

Haircuts, oil changes, vehicle inspection, vehicle registration, clothes, personal property tax, doctors appointments (if you don’t use flexible reimbursement), gifts, and vacations.

If you have room in the budget, you can add things like entertainment, date nights, kids sports, or even a “blow money” fund into your budget.

The easiest way to save for funds is to open as many bank accounts as needed. We have eight bank accounts for things like “Vehicle Expenses” and “Vacations”. That allows us to put aside a small amount every month to have a large amount available when needed without the risk of keeping cash in the house or the confusion of having everything in one account.

Step 6: Decide about Retirement.

If you don’t already do this, contributing to retirement will be your first goal after creating the budget. We need to set the amount now, though.

In “theory”, it would be smartest to pay off all credit card debt first before you start saving since your return on your investments in unlikely to be as high as interest on your credit card debt. However, if you’re having trouble keeping your finances straight, then forcing yourself to contribute to a Roth IRA (mine through USAA starts at $50.00 per month minimum contribution), forces you to save.

In the event of a true emergency, you can take contributions out (but not profits), and if you take every penny you have and pay off debt, there is no guarantee that you won’t just run up that debt again, undoing all of your hard work.

Start contributing to retirement right now, unless you’re in a unique situation where you’ve already paid off a ton of debt and plan to be debt free in the next few months.

If you contribute to retirement, add this to your budget. (If you contribute pre-tax, there’s no need to add it to your budget).

Step 6: Add in Necessities.

Are there any other things you need to buy every month?

If you drive a car, you’ll need to buy fuel at least monthly. Factor in how much you need to pay for fuel. If you’re not sure, check fuel purchases in your online bank account for the last 30 days.

Determine what your costs are to run your household. Do you ever think of the costs of all the little things needed to run your home? Shampoo, conditioner, body wash, hand soap, laundry detergent, deodorant, light bulbs, batteries, etc? Without being able to predict the cost of these things, a workable budget is a pipe dream. You can head over here and follow the instructions to create a home stock room inventory and price list. Determine the dates that you will stock up (I go for every three months), write down the total cost and the dates of your stock up trips.

If you’re not sure, aim for monthly and then go from there. What do you need right now to run your home for the next month? Shampoo, conditioner, toothpaste, garbage bags, etc. Set an amount monthly to purchase all fo the things you need to run your house and enter that amount into your calendar.

What if I buy all of my groceries and household items together? (Commonly done at Walmart, Costco, and Target?)

Easy! Just combine the categories. Instead of having a “Grocery” and “Home Supplies”, you’ll have “Grocery and Home”.

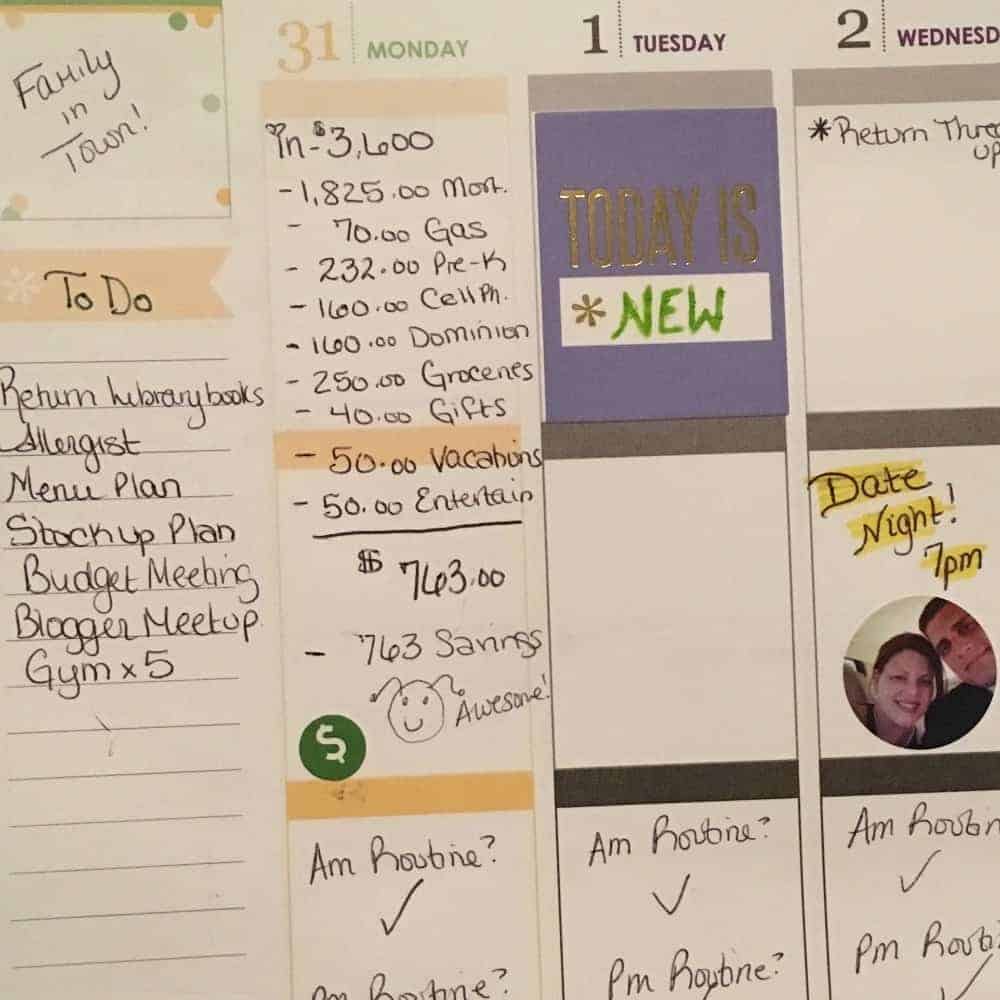

Step 7: Create a Calendar Budget.

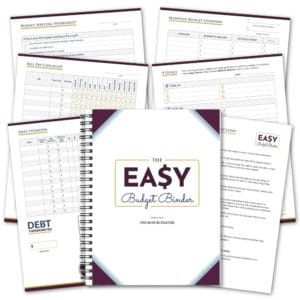

Go out and buy a 12-month calendar with giant writing blocks. The one in the photos is an Erin Condren Life Planner, which are gorgeous and popular but pretty expensive. This one from Me & My Big Ideas is AMAZING and way cheaper.

Do the following steps in pencil:

In your calendar…

Write in your pay days, then on your paydays, list the estimated income and list your bills.

Go through your list of necessities and start adding those amounts in on your pay dates preceding the date the money is needed. For gifts, leave at least a month before the event. For instance, my dad’s birthday is on Halloween (October 31st for my foreign readers), so I’m going to list $15.00 on September 1st to buy Dad’s birthday present.

Your budget will be tracked on your payday blocks. If you need additional squares, you can spill over.

Subtract the amounts of each bill/necessity from the income.

What if I don’t have anything left after bills and necessities?

If you don’t have anything left, go back to your lists of bills and necessities and figure out how you can reduce your bills for a while. Cancelling cable is the most bang for your buck, plus it forces you to spend time together and (gasp!) talk to each other!

If you need to make up money, selling things on Ebay is a great option. I’ve done this before and it’s a wild success every time. Take the free selling tutorial first.

Sort through your clothing and grab all of the jeans that don’t fit you and sell them in a lot. Lots of clothing in the same size sell particularly well. Make the listing end on Sunday evening at about 10 pm ET (statistically the most active time for sales).

You can also fill in a small amount with Inbox Dollar earnings, or Ibotta refunds on groceries. You can see more ways to earn additional income here.

The leftover amount each date is your extra income.

Step 8: Goals and the Fun Stuff.

Have you and your family make a list of future goals that cost money. Vacations to Disney World, buying a larger house, opening a brewery, staying home to be with the kids full-time, a new car, living debt free etc. Assign a cost value to each item.

Now think of the smaller goals. Think of things like sending out Christmas cards (that costs money right? most likely it wasn’t in your necessity list), adding a few throw pillows to your living room, getting a new tool for your workshop, visiting your family in Kentucky, etc. Assign a reasonable value to those things. Have each member of the family pick their top 3 priorities.

List the goals in order, 1 being the most important, 3 being the least. Do you see a pattern? Are the same things in the top three? Together determine the family top 3 goals and the order in which they are achieved. For instance, if your goal is to purchase a house, you may want the Disney vacation first, since it will take less time to achieve that goal. Consider alternatives, maybe you would rather vacation somewhere less expensive so you can get the house quicker.

Next determine how strict on the budget you want to be as a family (we choose very strict, with the occasional late night pizza meltdowns). Work together to remind each other of your goals and how to stay on track. Seek other sources of income to create income for additional things that you may want (a blog, an Etsy shop, reselling items on eBay for a profit, etc.)

At the end of each date (the 1st and the 15th), write the first initial for your goal (like H for house), then write the leftover amount. That’s the amount in your “bank” for that goal. If you want to work on a few goals at a time, separate them out and distribute the amount as you please.

Step 9: Update Routinely.

MAKE ABSOLUTELY SURE that you keep track of your actual bank account as well as your bill calendar. If your hubby forgets that he bought something, your bank account will reflect differently than your calendar. Every Monday, review your account online and note any discrepancies from the budget, adjust that date accordingly. Updating daily is even better until you get used to doing it.

I strongly suggest a “cash only” budget if you’re new to budgeting. It takes the guesswork right out of this.

Make your transfer to savings on the last day of the month. I make mine right before bed. I transfer every cent in my checking account over to savings so I start fresh the next day with the new months income.

An added benefit of having your budget in your calendar is that when you check your calendar every day, it automatically reminds you to update your budget. This system works really well with a cash only system.

What’s Next?

Once you’ve worked with this system for a while, we can graduate to an online way to track your budget. You can find my recommendations here, but a pen and paper calendar budget is the best way to start if you’re new to budgeting.

You can grab the 90 Day Budget Bootcamp which is FREE right now!

How many times have you started a budget and had it fail?

I know exactly how you feel. You know you need a budget but you have no idea how to make one.

The budgeting gene skipped you, and you’ve spent your whole life struggling with how to make a budget. You’ve tried everything, budgeting apps, budget planners, monthly budget templates, budget worksheets, and even the Dave Ramsey budget.

If we are being totally honest, you might not even know how to budget money, or what is a budget? You might not know how to create a budget, separate things into categories, set a household budget, or track your monthly expenses.

Learning how to manage your money is a life skill. If you need budget help, or you’re struggling with sticking to a budget we’ve got you covered.

Managing money just got easier. We can show you how to set up a budget and ways to save money on a tight budget. It’s our specialty actually, and we can help you make a plan and keep your budget simple.

You can find all of our budget tips right here…

P.S. If you’re feeling like no matter what you do you can’t get your house under control (not to mention your budget!) we completely understand. If you are sick of spending all day “catching up”, only to have it completely trashed again in a few days, then you should check out our FREE training “Why Your House is Trashed: The 3 Step Shortcut to Transform Your Home For Good With No Extra Time” which will walk you through how to break that cycle once and for all.

The training will walk you step by step through the three foundational routines that will help you manage all aspects of your home no matter how bad your situation is right now.

Implementing this core foundation allows you to work with your personality (and your specific situation) to create a custom plan to manage your dishes, laundry, schedule book, meal planning, budgeting, and a cleaning routine in less than one hour a day. You read that right, ONE HOUR A DAY.

If you want to take it a step further, we can teach you how to automate a ton of stuff in your home (without paying for it), giving you back HOURS of your life (yes, even your crazy life!). Then once you get the foundation set, we move on to more complex skills like meal planning, budgeting, and cleaning.

This is a proven system that’s been field-tested by thousands of people. People that have tried everything and could never keep their house clean or stick to a budget.

Like Jenn, who said “I used to struggle with absolutely everything. I married a man with 4 amazing kids and suddenly found myself drowning in dishes, laundry, and cleaning. There was NEVER enough money to cover everything and cooking meals that everyone would eat was impossible.”

“Then my dad got cancer and I also became his caregiver. The house and my stress level went from bad to worse overnight. I got the Hot Mess to Home Success course in desperation sitting in an ER waiting room at 3 am. I thought there was no way it could really help me since my situation was so unique with 4 step kids and being a caregiver for my Dad.”

“I had probably always been a hot mess, but this was a whole new low for me. Fast forward three months into the course and I meal plan regularly and stick to it (that’s never happened before), I use a planner every day, chores are a breeze, I have no dishes and laundry backed up (!) and I have significantly more time to do the things that matter (like helping my family battle cancer). You don’t even realize how much of a difference this stuff makes until it becomes your lifeline. I can’t imagine going back to how I used to live and I’m glad I never have to. I’m really grateful for that 3 am purchase!”

If you are ready to get started, you can sign up for the FREE one-hour training “Why Your House is Trashed: The 3 Step Shortcut to Transform Your Home For Good With No Extra Time” here…

How to Start a Budget

90 Day Budget for Beginners Boot Camp

What to do when you can’t pay your bills

One Weird Trick to Stay Under Budget (Every Single Month!)

The ONLY Budgeting Program You Should Use if You Live Paycheck to Paycheck (Hint: It’s Free!)

What To Do When You Go Over Budget

The Family Budget Three Steps We Took First To Start Paying Off Debt

The Family Budget Meeting: The Step-by-Step Guide

How This Family FINALLY Got On Track To Be Debt Free in a Year

Income Problem: What to Do When You Don’t Make Enough Money.

How to Budget Money on a Low Income.

Home Budget~ Budget Help

Good Budget Apps

Get More Done with 24 Time & Money-Saving Smartphone Apps

4 Money-Making Apps to Help You Teach Your Kids How To Save

How to Build Savings: 15 Awesome Money Saving Hacks

How to Find the Best Budget App to Track Your Budget.

The Ultimate Guide To Money Saving Apps

4 Reasons Why You Need The Every Dollar App

Ibotta Review: Is it worth it?

Budget Hacks: 7 Best Online Budgeting Tools

Best Way to Budget For The Holidays

Cheap DIY Christmas Gifts That Don’t Suck

21 Christmas Traditions To Enjoy On a Tight Budget

Cheap & Easy DIY Christmas Decorations

Give the Gift of Experiences, Not More “Stuff”

Cheap DIY “Year In Review” Christmas Ornament

$10.00 Family Christmas Tradition

The Perfect Christmas Gift for Couples

How To Budget For The Holidays

20 Gift Basket Ideas For Every Occasion…Thoughtful, Cheap and Awesome!

10 Cheap and Easy Thanksgiving Centerpieces

How to Save Money on Your New Years Resolutions…

17 Best Father’s Day Gifts (from FREE to $20 or Less!)

Last Minute Cheap DIY Halloween Costume Round-Up

How to Save Money Better

What To Do if You Need Money NOW

8 Ways to Build Your Debt Snowball and Pay Off Debt Fast

Creative Ways to Save Money: Live (Just a Bit) Simply & Save

5 Times That Being Cheap is Crazy Expensive…

Super Simple Citrus DIY All Purpose Cleaner! Save Time and Money!

Three Uncommon Ways to Save Money Right Now

Organizing on a Budget: 8 Clever Tips That Won’t Break the Bank

12 Budget-Friendly Family Vacation Ideas: How To Plan a Vacation on a Budget

Top 10 Biggest Budgeting Myths: Debunked!

How to Make-Over a Room on a Budget

Cheap and Unique Summer Bucket List

The Three Steps to Saving on Home Upgrades

What We Buy Now That We Can Afford It (and What’s Still Not Worth It…)

Spending Freeze Rules (and How to Save a Quick $1,000!)

How I Found the Cheapest Wedding Dress

10 Ways to Kill Impulsive Spending That Actually Work

How to Budget for a House: Saving for Your First Down Payment

Style on a Budget: How to Dress Like a Million Bucks (Even if You’re Broke)

How We Print For Free: Print for Pennies with the Staples Paper Sale!

8 Home Office Ideas on a Budget (+ pics of MY Home Office!)

Summer Savings: 12 Tips to Keep your Budget from Burning Up

Save on Late Summer Travel: Last Minute Trip Ideas (On a Budget!)

The Best Way to Save on Home Insurance

7 (Cheap!) Ideas to Make a Birthday Special

Stretch Your Budget with 40 Money Saving Tips You Haven’t Tried Yet

The Simplest Way to Reduce Grocery Spending (and Time in the Kitchen!)

How to Buy Any Car on Any Budget

When and How to Ask for a Discount…

When and How to Ask for a Discount…

5 Important Money Lessons To Teach Your Kids

How I Stopped Overspending and Paid Off $90,000 of Debt.

Full Credit Sesame Review: Accurate Free Credit Monitoring

Top 3 Life Hacks that Save a Ton of Money

Top 3 Life Hacks that Save a Ton of Money

No Pain & No Gain! 8 Healthy Changes You Can Make NOW to Lose Weight

Apartment Decorating on a Budget: How to Make Your Apartment Feel Like Home

12 Budget-Friendly Back-to-School Tips & Tricks

6 (Cheap!) At-Home Family Fun Night Ideas

4 Ways to Make Money with Your Smartphone…That Actually WORK (11 legit apps!)

Hosting Family Get-Togethers on a Budget: Fun Ideas for Bringing Families Together The Ultimate Budget Date Night

The Ultimate Budget Date Night

The Easiest Way to DIY Your Taxes

How to Hire a Professional Negotiator to Reduce Monthly Bills Without Paying a Dime Upfront.

Should I Get a Personal Loan To Pay Off My Car?

Girls Night In Ideas: $0 Make-Over Party and other Fun Party Ideas for Women

How to Start Couponing The Easy Way.

5 Budget-Friendly Ways To Honor Service Members.

The Ultimate List of Budgeting Printables From Pinterest

How to Afford to Be a Stay-at-Home Mom: 8 Resources You Can’t Live Without!

Sticking to a Budget When Your Motivation is Zapped: 6 Steps to Success

Budgeting for a Baby: Money-Saving Tips for New Moms

7 Essential Life Skills For Kids That Make Successful Adults.

The Only Home Management System That Worked For Me.

The Only Home Management System That Worked For Me.

25 of the BEST Things to Do in the Fall for Under $15

The art of saying No to friends when you need to save money

4 Easy Steps to Stop Fighting About Money Forever

My Completely Honest Review of Ting Cell Service (and how I saved $111/month!)

My Completely Honest Review of Ting Cell Service (and how I saved $111/month!)

The 3 Ways You Can Save On Every Car Repair (when you don’t know how to fix cars).

What Does Your Bad Habit Really Cost You? This is The True Price of Smoking and Fast Food.

10 Fun Things to Buy That Pay for Themselves (Plus Some!)

3 Ways to Save on Medical Costs (and How We Budget For Medical Costs)

A Sample Budget to Help You Create Your Own Budget

The 3 Personal Care Items You Pay Too Much For

How We Score Free Photo Books Every Year…

3 Ways To Get Free Kids Clothes… Every Year

Organizing Tools for Every Budget

Should you help your adult child with money?

5 Ways to Live Healthier on a Budget (with steps you can take right now!)

How to Get Huge Discounts on Household Products at Target

Top 10 Stupid Things That We Waste Money On

How to Instantly Improve Your Finances

How 14 Bank Accounts Saved Our Budget

WHY PHOTO GIFTS MAKE THE BEST FRUGAL GIFTS

I pay $41.00/month for my iPhone Plan! Ask me how:)

The Secret to Saving Money When You Don’t Have Willpower

The Simplest Way to Save on Groceries

The Easy Way to Save on Groceries (over $13,200 a year!)

10 Surprising Things That are Cheaper to Buy Than to Make

Save $400/year by switching your paper towels for cloth!

The Gift Cycle Method: How to Buy Gifts for Less!

6 Step System to Decorate Beautifully on a Budget

The Chopped Onion Project. Is there a limit to cutting costs?

Costco Membership for only a few dollars!

How we reduced our spending by $23,537.00 in a year (Money Saving Tips)! Financial File Cabinet: Organized and Easy to Keep Up.

Financial File Cabinet: Organized and Easy to Keep Up.

How to Save Money on Vacation… One Family’s Unique Solution.

This post may contain affiliate links. If you click & make a purchase, I receive a small commission that helps keep the Busy Budgeter up and running. Read my full disclosure policy here.disclosure policy here.

Good morning Rosemarie,

I just love reading your blog and using your tips daily. I am a recent college graduate/new homeowner and your tips have been a lifesaver! I wanted to know if there was a way for us to be on the same Ibotta team if I already have the app?? I would love for us to be able to help each other earn those bonuses!

God Bless,

Jordan

Thanks for keeping it simple and the resource links available. Now I need to put this concept inaction!! Here I go; thanks for the launch.

Anytime Shonna!

What if you don’t get paid on the 1st & the 15th? While I do get paid the 1st & 15th, my husband gets paid every Friday. How would you document that?

This is really awesome, thank you! I’ve tried for two years to figure out a way to budget that made sense for us but it only lasts a few months & then we fall off the wagon. I think this will make it much more do-able!

I have only recently started this so if you have any questions just let me know! But I work two jobs and one I get paid weekly and one I get paid biweekly. On my blank budget sheet I put 1st, 2nd, 3rd, 4th weeks and list all my bills and necessities where they would be due. I know my credit card is due the first week and my rent is due the last week of the month. For all other bills I just place them in their corresponding weeks as close to their due dates as possible (always good to pay early!) on my calendar budget portion I write what I am getting paid each week (those biweekly pay days are wonderful) and then list all the bills that I need to pay (from my paper budget) if I have any leftover I take that amount and add it to next weeks as long as that is what matches my bank account. I am still working out the kinks but if anyone else has suggestions or tips I would love to hear them! Hope this helps and just let me know if you have any questions. =]

What a good article I pinned it so I can go over it again and not loose it, also thanks for the links Great Article thanks again donita

I’m happy to help Donita! Budgeting takes a bit to learn but it’s one of those skills that will serve you well your whole life. Good luck!

Happy to help Donita!

While in my 20’s I had a fantastic budgeting system that allowed me to pay my bills, have money for savings and also have money for the things I wanted. While that is all fine and good, my paychecks were awesome for someone my age who is single and childless. Losing this job and being unemployed for almost a year threw me off track and now I am working for less pay full time and retail part time. My budgeting has hit a low, while I used to be so good at managing my money, my severe life changes have burned. I am still trying to recover and I hope that this system will help me pay off my debts and secure some money for a down payment on a house. Thank you for your tips and making it sound easy.

I am struggling with organizing my budget. My husband gets paid weekly. Some of our bills do not have an exact due date. How can I work this out so that I am not strapped every week?

Rude.

Hello! I have failed like ten times at budgeting.

I have just discovered your blog in Pinterest, searching for solutions or explanations on how make a budget. And I think this post is just perfect (at least for me) for beginners at budgeting, it’s a good summary of the important points, and now I realize what thing I was doing wrong. But the most important is CONSTANCY, thank you for remind this and give advice for what is the best moment.

I will follow your blog.

I just want to say, I haven’t tried your method yet BUT this is the first time I’ve ever read a “save your money” blog that I felt like I could follow!! Your struggles before sound a lot like mine now. I just happened to come across your “how I made Pinterest my full time job” on Pinterest. I honestly scrolled past it but had this little feeling I should read it. I have read so many of these types of blogs and they are all the same! Not yours! I finally found one I can follow! One I can understand! I’m so excited to get started and to read everything on your entire website!! Thank you so much for what you do, and are doing! Ahh!! I hope this helps my family and I!!

Reduce Stress with Budgeting Software or Creating a budget and sticking to it can lower your debt and erase stress,- I use Geltbox money -automatic download from any website (banks,credit cards).

I like that I can keep my data locally instead of in the cloud.

An excellent home finance planner and tracker.

Hello! Finally, a budget that interests me enough to try it 🙂 I’m curious, is there a link to view your entire calendar? Just a sample month. Thanks so much!

Great Idea! Thanks for sharing 🙂

I love everything about this Rowy! 🙂 Budgeting using a calendar is the best and easiest way to make your budget work for you!

If you aren’t about saving money and being money savvy, then why are you here?

Hi,

I love your blog!! Your steps are so easy to follow. Would you do a blog post on 15 minute vegetarian meals under a budget?

Thank you

You make it all look so easy! I absolutely love all of your ideas and your site is super friendly and easy to use I love it!

My husband gets paid every 2 weeks. I have never been able to figure out how to budget because dates change constantly. Please . We are excited to start this. Thank !

We are on a two week pay as well. Take a calendar and write in you paychecks on the appropriate day. Go through all your bills and write them in the appropriate date. A day or two before payday write down all bills due for the upcoming two weeks

Some of the best gifts are from the heart and cost nothing on money value.

I am new to budgeting after a lot of spending and i am looking forward to using this guide, but i have a question I get paid once a month usually on the last day of the month how do i make my budget?

I basically needed someone to tell me step by step how to get started, and that’s exactly what you have done. Thank you so much!

You bet! I’m so glad it helped 🙂

How long did it take to pay off your debt?

I was so happy to see this article and know that I was right on track! I did the same as you did and I first put my income and expenses to pen and paper. After a while, I added it to an excel spreadsheet. Now I can plug in or take away any expenses and the program keeps a running total for me.

I use the Google Calendar to keep things on instead of a regular paper calendar but it works great for me. I really hope people take your advise to heart because it really works. You find out exactly where you stand and what you need to make changes to. Thanks again!

Some people are on a very low fixed income. They are lucky to be able to afford $15 per person for birthday gifts, depending on the amount of people they need to buy gifts for. In those cases, being a mother of 3 and having raised 3 of my nieces and nephews, I know that I would be happy with a dollar store gift if that is all they could afford. I would be happy that they tried to get me anything. I think that making comments on the amount Rosemarie put down for her fathers gift is rude and unnecessary, Sylvia. Rosemarie is trying to show people a better way to budget and people like you make it uncomfortable for her or any other blogger to want to help anyone. Please think about what you are posting next time and who you might hurt in doing so.

Your article recommends doing funds by opening as many bank accounts as needed. Where do you open all those accounts? Do you use just one bank that lets you string together a bunch of accounts? Thanks!

I would love to see more photo examples using this method. I’m a visual learner!

I agree!