When you have an income problem instead of a spending problem, traditional budgeting advice can drive you nuts.

“Just skip the Starbucks every day and you’ll be a millionaire!”

Umm, yeah. Not helpful.

Update: 4/5/20 I know how stressful finances are right now with stay at home orders and the pandemic. I also know that I’m uniquely qualified to help you. I’ve helped hundreds of thousands of people get out of the paycheck to paycheck cycle (after trying and failing for years), by teaching them how to work with their unique personality to actually stick to a budget.

I’m giving you access to the insanely popular 90 Day Budget Bootcamp for FREE. Because I know that this program will change every aspect of your life. Take a look around. Because this is the LAST DAY you will ever sit around worrying about money. Let’s get to work.

Join the 90-day Budget Bootcamp for FREE here…

That’s why I asked Kara Fidd of Simplifying DIY Design to guest post today…

Because that was exactly Kara’s problem when I met her. And Kara is a wealth of knowledge about how to deal with an income problem.

And most of these very simple changes are outlined in the 90 Day Budget Bootcamp which you can grab FOR FREE here…

I have always been extremely motivated by other people’s success stories, while I was going through my own financial journey because ALL I wanted was a job that would let me stay home with my kids.

For me, that was the driving force behind our ability to reduce our spending by over $23,000 a year, pay off over $35,000 of debt, and for me to find a way to make my old salary from home.

Here’s what Kara had to say…

How to Deal With Your Income Problem.

I felt like I was drowning.

That’s the best way to describe it at least.

It felt like it was happening all at once. I met the love of my life, we got married, he joined the Air National Guard and took a technician position, we had a child, and I became a mostly-stay at-home-mom (only working weekends when my husband or one of our parents could stay with our son).

The decision to become a stay at home mom was mostly personal but, I also didn’t make enough at my job that it would have made sense to continue working to pay for daycare. Losing most of my income and then the pay cut my husband took when first switching careers hit us harder than we expected and our savings account drained fast.

The money going out wasn’t matching what was coming in and I spent more and more time staring at the screen of my online banking hoping it would change. I’d get my calculator out and punch some numbers and then do it again. And, I could NOT figure out why we had so little money when we didn’t spend it on anything.

Except debt and bills.

But how could we get out of debt when we had no money left over? It was a vicious cycle and it truly felt like drowning.

I knew we needed to do something fast.

So I did.

It wasn’t easy (and it wasn’t always quick) but my life looks completely different now. I want to walk you through what we did right (and what we did wrong!) so that you can navigate this yourself.

We Always Stayed a Team.

My husband and I tried hard not to let this situation cause problems in our marriage. The decision for him to take the federal technician job was much more of a pay cut than we were expecting but we made that decision together. We also made the decision for me to become a stay at home mom together, so we made it a point to never cast blame or point fingers at the other person.

Because we made these decisions together, we knew we needed to face consequences together.

Staying united was so important.

We Compromised.

That’s not to say that we didn’t have problems. He liked to stop at a local gas station every day for coffee, snacks, and sometimes lunch. When I would ask him to stop doing that and he would get frustrated. Eventually, after totaling up what he was spending (which was $400/month) he agreed that he needed to cut back.

We tried a cash allowance so that he could still go to the store but when the cash ran out, he would just start swiping the debit card again. After a while, he gave me his debit card so that he wouldn’t be tempted.

I cut back everything.

We were already really conscious about what we were buying. I never bought myself anything, and neither did my husband. We sold pretty much anything we had that we could live without and we bought our son only the bare essentials– food and clothes.

I still remember his very first Easter and his basket was filled with toys he already owned because we couldn’t afford new ones.

(Hint: He survived just fine and so did we).

We Used Substitutions.

My trick for baby clothes was consignment stores for a while until I realized that Old Navy has a killer clearance section. Many of the deals I found there were cheaper than the consignment store! Some shirts were as low at $0.97! If it was a great deal I grabbed it regardless of it being a larger size and then I stored them on a rack in my basement.

We also canceled cable, went down to one car (which cut back gas expense, insurance, and maintenance costs), and stopped any and all “extras” like dinner out, coffee stops, etc.

We Got Financial Advice From An Expert.

In all honesty, I kind of lucked into this one because I found Rosemarie from the Busy Budgeter. Her articles are a goldmine of information, but it wasn’t until I got REALLY lucky and won a Financial Roadmap giveaway she was doing for a post that it really started to click for me. (My name in the Financial Case Study was changed for anonymity, but that’s me, Amanda!)

While I lucked into getting 1:1 financial advice from Rosemarie, she has a 90 Day Budget Bootcamp that’s amazing (and completely free) that walks you through much of the same process). But you could also bare all with a friend that’s good with money and ask their advice. Sometimes, it just helps to have an outside party take a look with fresh eyes and point you in the right direction.

That’s exactly what she did for me. I’ll never forget what she said after we went through our finances and bank statements with a fine-tooth comb. She said, “Kara, you don’t have a spending problem. You have an income problem.”

We Tackled Our Income Problem With A Side Hustle.

Finally! An income problem! That was exactly it. That was also exactly why I felt like I was drowning!

My husband was working 2 jobs, I was working all the spare minutes I had between my weekend nursing job and trying to make money from home (I had started a blog and an Etsy shop along with other smaller things like surveys and using rebate apps).

What else could I possibly do? Hint: There’s a lot you can do!

I actually started making money from home

While making money from home sounded like the best idea ever, it was a lot harder in practice. I tried a lot of things before I hit the jackpot.

Since I had already started an Etsy shop to make handmade items, but I was spending money to make them and it took so much time to create them and ship them that in the end, I was making very little profit for hours of work.

I knew I needed something that could tackle my income problem, make me more money with less time spent, so I turned to blogging.

After spending hours on it, but I wasn’t making very much progress.

I Used The Skills I Already Had To Make Money From Home.

The turning point was when I started using my natural skills. When Rosemarie was working with me for the Financial Roadmap she took a look at my blog and asked, “How much are you spending each month in graphic design services?”

I thought that was hilarious because I could barely afford groceries so why would I be paying a graphic designer? “Nothing, I make them myself” I responded.

Turns out, I’m really good at graphic design.

She laid out a plan of how I should focus my effort on the things I’m exceptional at. She said bloggers pay people to make their graphics and I could do that. It seemed like a good way to supplement our income problem.

Eventually, because our styles were so similar I started doing graphics for her and some other clients. Around the same time, we moved into an apartment that was much closer to my husband’s job (to reduce gas expenses even more) and found out we were expecting a second child.

I declared that by the time our second child was born, we would be financially stable.

And we were! Plus, my husband was able to land a better position with the Air National Guard that gave him active duty pay and benefits. This was a huge help financially and as a bonus the need to work two jobs is finished.

We Only Did The Things That Matter.

As the blog started growing I was also able to quit my weekend nursing job which helped me dedicate more time with higher ROI (Return on Investment) tasks with my blog.

Making money creating graphics allowed me to re-invest in my own blog.

Eventually, I switched gears leaning even more towards my passion for design. I started a new blog that focused on design and teaching bloggers that couldn’t afford graphic designers how to do it themselves with easy to use tools and templates.

Because I knew my target buyer (avatar) so well that everything blogging-related I had learned from Rosemarie just clicked. I took on more client work for a while. After about 6 months, I launched a product that generated just under $11k in one week! I couldn’t believe it, I was actually making money from home!

We Stayed The Financial Course (Even When We Had Money).

We used the income wisely.

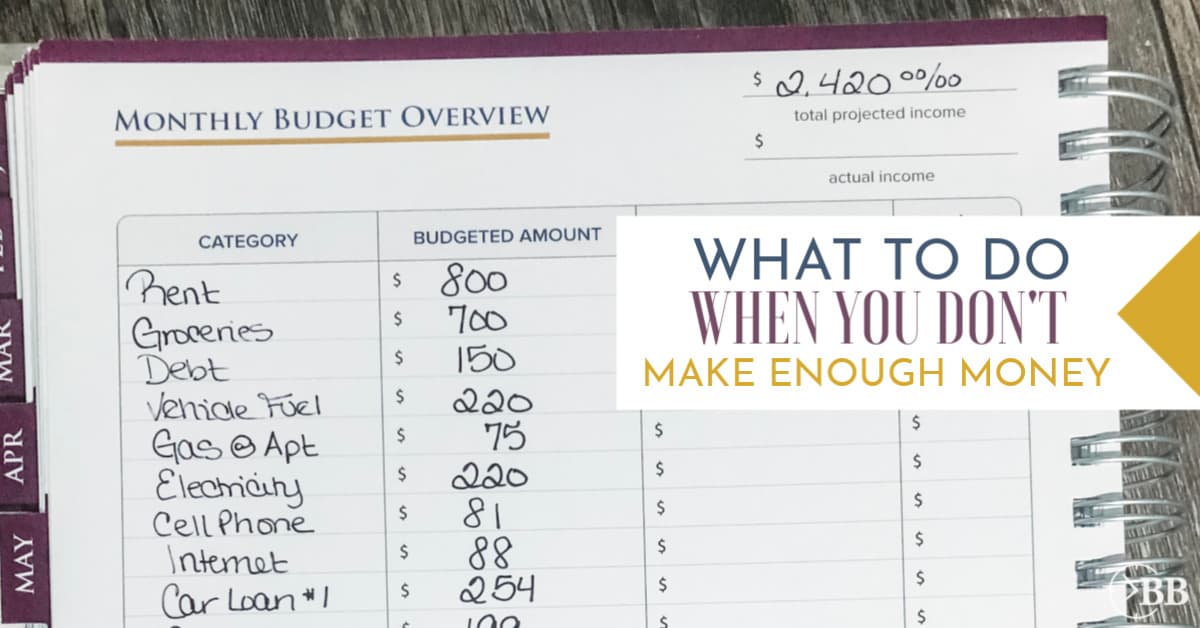

I came up with a system for our budget that worked for me. After implementing Rosemarie’s Budget Bootcamp which walked me through how to start a budget step-by step, I was able to take the concepts she taught and make them work for my family.

One of the concepts that helped a lot was having a hard to reach bank account. While ours isn’t exactly hard to reach, I found it was helpful to simply not have “extra” money sitting in our main checking account. I was able to open up several accounts with USAA and use them as sort of a digital envelope system.

When my husband got paid, we would pay all of our bills with his first paycheck and then used the second paycheck to pay rent for the next month (this ensured that we always paid on time and early).

Then, any leftover income I made (after paying expenses, setting aside money for taxes, and any investments I made that month) we would put that straight towards debt. Each time I launched a product I was able to knock out another debt. As the debt went down, the money we had leftover each month went up and we were able to put more and more towards the debt.

We did not focus on a savings account during this time. We only started saving money when we decided we wanted to buy a house.

Guess who was able to save up an entire down payment in a little over a month?!? That’s the power of a blog and a good budget!

We Established Routines That Supported Our Efforts to Save Money.

We learned that money and home routines are connected… it’s hard to budget unless you are organized.

We learned that money and home routines are connected… it’s hard to budget unless you are organized.

When we were struggling, I really felt like a complete mess. Everything was so unmotivated and down. I was always behind on dishes and laundry and anything else around the house. I was spending all of my time either blogging, making graphics, or being with our kids.

The mess around us was so frustrating and I blamed myself. My husband helps with household duties but somedays we were both so exhausted, that it just didn’t get done.

Every day ended with not keeping up, which left us further and further behind…

Getting the Dishes and Laundry Under Control.

This started turning around when I was going through Rosemarie’s 90 Day Budget Bootcamp.

She explains a simple dish system that I could actually do (even with my hectic schedule). This was something I was seriously implementing when my husband went away for military training. I knew he wasn’t home to help out, so I had to make sure I stayed ahead.

Fun fact: if things even start looking slightly out of control I will get overwhelmed and just not do it at all.

Anyway, I did the dishes every single night. This way each morning I woke up to NO dishes in the sink. I immediately unloaded the dishwasher while my kids ate breakfast so that I could continuously load it as the day went on.

We also got rid of all but one of our laundry baskets (we had 5, not including our hampers). Getting rid of the laundry baskets meant that we couldn’t let clothes pile up, then run them all at once just to have 5 baskets of clean clothes sitting there unfolded because we didn’t have time to fold 5 baskets of clothes.

I ran the laundry as soon as that one basket was full (about every 2-3 days). If I would wash, dry, and immediately put it away, it worked. I didn’t allow myself to do another load until that was all done so I had to make sure I did the whole process from start to finish.

I was determined to establish a routine so I could get caught up with the dishes and the laundry. That step is huge for me. I was able to get it done and not feel like it took up hours of my time to do so. Doing a little at a time was the only way I could be consistent. It never felt overwhelming when it was just one load or a couple of dishes.

We Stuck with The Changes That Made A Difference.

Making progress on the finances and our income problem helped the house too.

Making progress on the finances and our income problem helped the house too.

When we were able to start paying off debt and climbing out of the hole, I found myself so much more energized. I finally felt a sense of relief since I was working less and felt so much more motivated. I was able to keep up with household chores and actually have fun with my kids.

Every situation is different so figure out what works best for you. There isn’t a “one size fits all” solution for everyone.

We went from overwhelming debt to buying a home for our family in a few years by cutting back anything and everything we could along with finding ways to make more money.

We were never going to get anywhere unless we made more money. I thought about what Rosemarie said, “we don’t have a spending problem, we have an income problem.” Right after that, my husband got promoted to a position that paid more and had better benefits.

And I started building an online business that I could scale. I wanted to build a business that didn’t require trading time for money. A business that had very little overhead costs associated with it (like inventory or materials).

We Attacked Our Debt

That was our goal. We created routines and systems in our house and our finances that helped us pay off debt quickly. And, once the debt was paid off we were able to save for the things we wanted like vacations and a house.

It made us feel like we were never going to get out. However, we also learned so much about ourselves, our marriage, and what we could really push ourselves to do.

I wouldn’t change it for the world.

If this is you, and you have an income problem… your solution may not be graphic design and blogging. But, you can still work together, stay on the same page, have consistent effort and think outside the box of scaleable side incomes using your specific skills and abilities. Rosemarie actually has an online training called Make Money at Home Master Plan that teaches you how to use your skills and abilities to find an at home job that works for you.

And, get the 90 Day Budget Bootcamp and start working through it. The Bootcamp is completely free and is a great place to start getting your finances under control.

P.S. If your income problem situation is worse and your ability to get yourself or your family the basic necessities are compromised, there are programs that can help you. I completely understand that not all income problems are the same. The first step is to ask for help. 411 is a national service that matches people with assistance in the area that they live. There are also government programs that can help you… Never be afraid to ask for help.

Kara is a wife and mom of two. She owns Simplifying DIY Design and teaches bloggers how to create graphics to grow their blogs. She enjoys spending time with her kids, traveling, and watching murder documentaries on Netflix. You can find her at simplifyingdiydesign.com and if you happen to be a blogger looking for some awesome free canva templates just click right here.

I absolutely love this article! I have so many friends and family who really struggle with their budget and I now realise that most of them have already cut their expenses to the bare minimum, they just need to find what they are good at and turn it into an income! I think that is the most difficult part. Can’t wait to explore this site in more detail.

Great insight! Even as a full-time blogger with passive income, falling short of sufficient income just recently happened to me. I was severely ill and on bedrest for 3 months, which cut down my income by a lot since I was unable to do any sponsored work. Right now I’m trying to figure out how to catch up, which probably means selling other services of my other areas of expertise. Thanks for sharing this – I really needed the inspiration and motivation to catch up on my finances!

This post hits me so hard right now, since I was fell ill and was unable to work for about 3 months and basically cut my income in half. I can relate to the part where you mentioned about feeling guilty when the house is a little messy – I feel like I spend so much time playing “catch up” with work that the house is a mess, and then I feel awful because I can’t put all my energy and focus into two things. But I’ve actually started doing the same dishwashing trick you mentioned about a month ago and it helps SO much! Great post!

I loved this article . I have a good job and really like what i do., but for years have wanted to find a side hustle to help get me out of debt and just be able to be financially stable. I have spent the past 6 months researching blogging and hope to soon be confident enough to actually get started.

This post is so helpful right now. Sometimes I can get stuck in only one way of thinking about ‘money’. Either I need to save more and be more frugal….or I need to hustle more and make more money. When really, I need to do both for our family. There are so many great tips here and I keep clicking around. Thank you!