If you’re asking yourself, “How many bank accounts should I have?” Then you’re smarter than most people.

Because most people get a checking account to spend from and a savings account to save money for large purchases (or to act as an emergency fund) and call it a day.

And if you’re insanely organized, amazing with money, and a master budgeter… then that’s really all you need (just make sure the savings account is a high-interest savings).

But I would argue that a master budgeter isn’t typing “how many bank accounts should I have” into a search bar.

So if you’re asking yourself “how many bank accounts should I have?” then that means that you aren’t like most people. And you’re realizing that there may be a smarter way to manage your money by using additional bank accounts or you’re a total hot mess when it comes to budgeting and have no idea how to get started.

If that’s the case, then I can help you.

Multiple Bank Accounts Make Managing Money Easier.

Let me walk you through the bank accounts I used to pay off over $30,000 worth of debt as I completely transformed my financial life and why I think having multiple bank accounts will change your entire life.

Because I used to be a complete hot mess.

I always spent more than I made, my credit score was trashed, I had over $30,000 in debt, and every time I tried to budget… I ended up right back living paycheck to paycheck (often times even worse!). When I finally unlocked the secret to working with my natural personality (instead of against it) I was finally able to set and stick to a budget. Everything changed (seemingly overnight).

I reduced our spending by over $23,000 a year, I paid off our debt of over $30,000 and I was able to quit my job to stay home with our kids. I was able to make up my salary from home by running a home daycare.

After trying and failing to change our financial future for over 12 years, it became… easy. Not sitting on the couch eating Cheetos easy- but certainly easier than anything else I had attempted. And it actually worked.

It’s been working for over 9 years now and counting…

You Should Have A Minimum Of Three Personal Accounts.

These three accounts used to actually be the standard best practice, but now there are banks that let you do a digital cash envelope system directly into your bank account. Which is both extremely effective at naturally reducing spending but also makes budgeting extremely easy since you no longer have to track your spending… I’ll cover that in the next section. So the three account system is no longer considered the best practice, just the minimum amount you need.

Personal Account #1: Main Checking.

This is where your bills come out of and where you spend most of your money with a debit card.

Personal Account #2: Check Hold Account.

This is a separate checking account at the same bank as your main checking. When you write a check, transfer money to your savings, or to another bank… transfer the money here first. Any bill pay should happen from here too (not automatic bill pay though). Any checks you write should come from here.

This means that your main checking account balance is always correct and isn’t reflecting that you have money that’s already been spent via check or transfer (that just hasn’t updated).

This is the number one secret to never over drafting your account (I explain in the video below why that works so well).

Personal Account #3: Off-Shore Savings.

Despite the sketchy name, this isn’t really an offshore account to embezzle money. It’s what we call the “hard to reach” bank account where we hold our emergency fund.

This account should be a high yield checking or savings (Both Capital One 360 and Ally are great for this) but don’t get a debit card for this. Make it so that the only way you can spend money from this account is by transferring the money back to your main checking account (which should take 2-3 days).

That makes it so it’s a pain in the rear to be able to use that money. And there’s a 3 day cooling off period while you wait for the transfer to take place. This gives you time to decide if you really need this. By keeping our main checking account “poor” and our savings a pain to access- we grew our wealth easily despite being chronic over spenders. (There’s a lot more to it than that- we had to learn how to work with our personality to conquer our budgeting skills- You can just grab the printable we used to do that here).

It’s one of the most successful ways for people to not use their emergency fund.

6 More Personal Bank Accounts You May Want:

Most people who used to suck at budgeting and taught themselves to manage their money well use multiple bank accounts (we used 14 accounts for years) that let’s us earmark money for how we plan to use it. Here’s the additional bank accounts we’ve had at various times…

Annual Bills Account:

For paying quarterly or annual bills like vehicle insurance, HOA dues, property taxes and trash service.

Blow Money Account:

We use a life changing method to incentivize savings that’s been the key to our financial success. Traditional Budgeting requires you to have a ton of willpower and to make good choices consistently for years until you see a reward. Which works for some people. We are not those people. After trying and failing that way for years, we discovered the power of working with our natural personality and incentivizing our budget categories… So we get to keep 20% of whatever’s leftover at the end of the week or month in each budget category. We then take the other 80% and apply it to either debt or savings.

So every week, we get to “win”, while we paid off massive amounts of debt. This instantly changes the mindset of a spender to a saver. Because the only way to get what you want is to be under budget. It also helps you spend money intentionally on the things you want most… not on whatever happens to be in front of you in a low willpower moment.

Jon and I each have a blow money account to spend on whatever we want. In the beginning- this was small amounts of money. As we got better at budgeting, more excited about incentivizing, and we became debt free- it grew into larger and larger amounts.

Vacation Fund:

This is a high interest savings account where we park money to go on the next vacation. In the beginning- this was small amounts for camping or weekends, but as we paid off debt and earned more blow money- we transferred some of that here for larger trips like Disney World and to renovate our RV (which gives us epic $500 a week vacations in Big Bessie– which is better than any hotel in the world).

Vehicle Fund:

When we finally got out from under our massive car loan by selling our car and using a tax refund to pay off the additional loan amount plus buy a cheap car for $5,000, we left behind car loans forever. We use this smart system of buying a car under kelly blue book value and then selling it a year later for more than we paid for it- then buying another car (again under Kelly Blue Book Value) and repeating that process every year or two. Our cars are now worth $16,000 and $11,000 but they cost us nothing to drive every year (except routine maintenance). You can see how we do this despite not being very car savvy here.

Medical Fund:

We use this account to pay for prescriptions, co-pays and medical emergencies.

House Fund:

We use this account to do necessary home repairs, upgrades and maintenance.

Christmas Fund:

I funded Christmas entirely through Ibotta Earnings (a couponing app that let’s you instantly save on generic items like milk and cheese without needing to buy a specific brand) while we were paying off our debt, but then we set up a Christmas fund, where we would set aside money every month so when Christmas came, we had extra money set aside for it. Which really makes the month more jolly!

Digital Cash Envelopes Changed Everything- We Use Qube Now.

I used the above accounts for years successfully and taught hundreds of thousands of readers how to do that as well. Until 2021, this was the best way to set up your personal bank accounts. In 2021 though, Qube Money launched the first successful digital cash envelope system that integrated right into your bank account.

This new technology has completely changed budgeting for the better.

I’m convinced that within the next 5 years, it will be standard practice to budget this way.

The only company that does this right now is Qube. You can sign up for a free account here, or read my in-depth review of Qube here.

The simplest way I can explain it is that you divide your money into Qubes (or cash envelopes) directly in your bank account- earmarking them based on how you plan to spend that money. So into categories like fuel, food, kids clothes, etc.

Then you choose which envelope to spend from inside the Qube app, swipe your card and the money is removed from that envelope only.

Qube has all of the benefits of cash envelopes (which has been proven to control your spending without even trying) and none of the drawbacks. Because it’s 2021 and a lot of our purchases are online and can’t be made in cash, it’s an extremely effective way to budget.

And because it’s a bank and budgeting app in one, you don’t need to track your spending or do maintenance on your budget at all. Take 10 min to set it up at the beginning of the month (or 5 minutes at the start of every paycheck) and that’s all you need to do.

Qube also gives you the power to create as many envelopes as you need to earmark money for whatever you want, with just one account.

So it helps you budget at the granular level, like creating envelopes for…

- “Chase’s birthday”

- “Kids waterpark trip on the 19th”

- “Date night on the 4th”…

When you look at your schedule while you budget, it helps you not go over budget. Because you can earmark money for events instead of scrambling when you forgot about something. I did a full review of Qube in the video below (or you can read my Qube review here).

But using Qube is the current best practice to budget easily and it’s what I use now. You can get a Qube account here (it’s free).

“How Many Bank Accounts Should I Have If I Use Qube?”

Main Checking Account For Bill Pay:

That’s whatever checking account you used before Qube. You could technically transfer all of those bills over to Qube and use their direct deposit to use Qube as your main account, but I don’t recommend doing that. It would take hours and is a pretty overwhelming job with virtually no reward. Just leave money in your main checking account to pay the bills that were set up prior to Qube. All of those get paid from here.

Off-Shore Savings:

This is witty name for our online only high interest savings account (we use Ally and Capital One 360). We use online only and shred the debit card to it so that the only way we can get our money is to transfer it to our main checking account, which would take about 3 days to do. That makes it fairly overwhelming to spend this… so we don’t. Which is a perfectly example of working with your personality.

Check Hold Account:

This is where we transfer money that’s going somewhere but will take a few days to get there and register with our bank. We use this acocunt to write checks (we just transfer the amount of the check here), and to make transfers to our savings account, investment accounts, and to Qube.

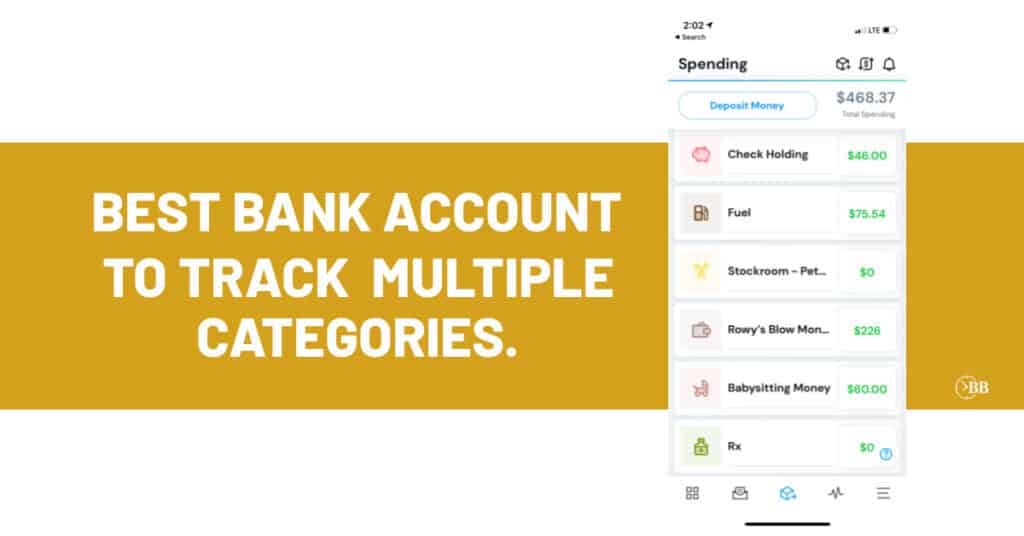

Qube Account:

Then in Qube, we have the following digital cash envelopes (and these can change frequently based on what’s going on in any particular month since the envelopes are so easy to create and delete):

- Rosemarie’s blow money

- Jon’s blow money

- Medical

- Savings hold*

- Food

- Food hold*

- Date night

- Child care

- Vacation

- Rowy’s hair cuts

- Jon and kids hair cuts

- Stockroom

- Waterpark

- Build the fire pit in the backyard

Free Shortcut Budgeting Workshop with Qube:

Hint: If you have trouble sticking to the budget, but you’re intrigued at how we use Qube to work with your personality to pay off your debt and give you a way to win with money ever week – then I’m doing a free workshop that will blow your mind. I teach you how to work with your unique personality so that ANYONE can stick to their budget the first time and every time.

It’s called “Shortcut Budgeting” and it teaches you how to unlock the power of our way of budgeting with the life-changing free technology of Qube Money. Reserve your seat here for our next virtual workshop.

“How Many Bank Accounts Should I Have For Business Accounts?”

It’s a book by Mike Michalowicz. It’s a very quick read (about an hour or two?) but if you implement what he teaches- it’s life changing.

Our business budget basically runs itself now with no needed input from me and it’s been incredibly successful for us for 6 years and counting. I’ll never do anything else.

If you do Profit First for business, you’ll need 7 business bank accounts:

Income Account:

This is where all of our businesses revenue gets dumped into.

Then on the 5th and 20th of the month, I transfer the following percentages from the income account to the following accounts (all in the same bank).

Hint: your percentages may be different- these are the percentages that work for my business.

OPEX (Operating Expenses) – 45%

This is the main debit card for my business. Salaries for employees, advertising, services, tech, and all other expenses get paid out of here.

Owner’s Comp- 30%

This is where my salary gets held. I transfer the same amount every month to my personal account (now Qube) and we live off of that .

Taxes- 15%

This is where money is transferred to be held for taxes. It’s immediately transferred to an “off-shore account” (that’s my term to describe a bank as being hard to access so I’m not tempted to use it- it’s not a foreign bank account) called “Tax Hold”.

Profit Account- 10%

This acts as an emergency fund for my business. Money immediately gets transferred to an “off-shore” business savings. (See description above, it just means hard to access so I don’t spend it) . Every quarter in January, April, July, and October, I get to take 50% of the profit account as a “bonus” in addition to my income.

Tax Hold- High Interest Savings

This is where the tax money sits long-term in a high-interest earning account (we use American Express Savings) until it’s needed to pay taxes. I don’t get a debit card or checks for this account. The only way to gain access to that money is if I transfer it back to this main tax business savings account. This is just where it sits and collects interest until taxes need to be paid.

Profit Hold- High Interest Savings

This is where the profit money sits long-term in a high-interest earning account (we use American Express Savings) until it’s needed to pay taxes.

On the 5th and the 25th of each month, I sit down to distribute money. That’s the ONLY maintenance I need to do for my business budget.

Hint: Suck at calculating percentages? Me too, I use percentagecalculator.net to do this easily.

Hint: I strongly suggest you grab Profit First the book, which is what this was implemented from, and give it a read (it will only take a few hours, it’s not long for the sake of filling up a book). And it will explain this system in depth.

But it’s incredibly life-changing. It’s one of the best things I’ve ever done for our business.

That’s the best way to use multiple bank accounts to budget successfully.

But if you just need to know the types of bank accounts available and who should use them. I can break that down here.

Types of Bank Accounts

Personal Checking

high yield checking (the highest rates are usually online only companies with no local branches like Capital One 360 checking Ally, and American Express Savings.

Personal Savings

High yield savings- best interest rates usually go to online only banks, but savings pays a little higher than checking although is limited to only 6 transactions a month.

Money Market Accounts

These are meant to be a higher interest savings account with the ability to write a check (or even use a debit card) but still having a limit on how many transactions you can complete in a month. But these are mostly antiquated with high yield savings accounts available now.

Business Checking

This is set up the same as a personal checking account, except that in addition to your name, your business name is listed as the owner. Because there’s less competition- there are often higher fees on a business account. You can talk to your accountant or tax strategist to see if you may be able to use a separate personal account instead of a business account to track your business spending.

Business Savings

Same as above. This is the same as a personal savings. The only difference is the owner is listed as the business in addition to your name.

Foreign Currency Bank

This is a special bank with either low of no foreign currency fees. They’re meant for businesses that deal with multiple currencies or that travel frequently to locations using other currencies.

Why Do People Choose To Have Multiple Bank Accounts?

While having multiple bank accounts may sound overwhelming, people usually choose to do it because of the opposite reason.

It lets you budget easily while still being mostly “hands off”.

If you’re the type of person (like 78% of Americans) that will find a way to spend extra money laying around…

Digital cash envelopes or multiple bank accounts give you the illusion that you have “just enough money” when in actuality, you have plenty of money socked away.

I jokingly call this “feeling poor but being rich” If I could easily see and transfer my savings account. I’d have already spent it in an impulsive moment.

When it’s out of sight, it’s out of mind unless you need it.

If you’re not an impulsive spender who struggles with budgeting, and you relate more to Mr. Scrooge who likes to swim in his money… then you may have multiple accounts to properly insure your money.

Since FDIC insurance caps at 250k, having multiple accounts at different banks helps ensure all your money is insured.

While just a checking and a savings account might work for some people, with over 78% of Americans living paycheck to paycheck…

Being open to the life-changing benefits of multiple bank accounts can help you easily budget while working with your unique personality and not against what your natural inclination is (to spend money).

Tools referenced in this article.

Get a Qube account FREE here (digital cash envelope bank and budgeting app combined).

Get Profit First the book here…

Grab a Capital One 360 account here…

Get An American Express Savings Account here….

Read More Like This

How 14 Bank Accounts Saved Our Budget.

How to Start a Budget When You Suck at Budgeting.

Qube Review: Best Budgeting App in 2021.

How we reduced our spending by $23,537 in One Year.

The 4 Side Jobs that Make Me Over $3,000 a Month as a Stay at Home Mom.

How will Qube work with the Target Red card?