Living paycheck to paycheck is a struggle. And most of the financial information out there doesn’t apply to that situation. If you attempt a monthly budget when you live paycheck to paycheck and spend too much in any week, you’ll overdraw your account, making your situation worse.

If you live paycheck to paycheck, there’s only one budgeting program (system) that I would recommend. It’s the one we used to claw ourselves out of over $40,000 worth of debt.

My days of living paycheck to paycheck are long over… and my sole purpose is now to help you leave those days in the past as well.

Update: 4/5/20 I know how stressful finances are right now with stay at home orders and the pandemic. I also know that I’m uniquely qualified to help you. I’ve helped hundreds of thousands of people get out of the paycheck to paycheck cycle (after trying and failing for years), by teaching them how to work with their unique personality to actually stick to a budget.

I’m giving you access to the insanely popular 90 Day Budget Bootcamp for FREE. Because I know that this program will change every aspect of your life. Take a look around. Because this is the LAST DAY you will ever sit around worrying about money. Let’s get to work.

Join the 90-day Budget Bootcamp for FREE here…

Or keep reading to get step by step instructions on the only budgeting program you should use if you live paycheck to paycheck…

Once you have your budget down on paper, you may be trying to figure out how to track your budget. You can track your budget with paper for a while (and I highly suggest you do), but once you get into the swing of things, it’s nice to have a program that tracks your budget more efficiently than you can on pen and paper.

They even have life planners now, that you let you track your budget right in with your schedule/organizer like the Living Well Life Planner.

If at any point, you find that once you start to track your budget on an app or a website, that you stop updating it, then abandon the app or website and go back to paper. The best way to track your budget is to use whatever method you will actually do. There’s nothing wrong with a paper budget.

Until 2021, there wasn’t a single budgeting app that I could recommend because they all worked so differently, results were often mixed, and none of them were easier than pen and paper… so they all had a distinct learning curve that made something that’s already overwhelming even more so.

In 2021 though, Qube Money finally released the only budgeting app that’s also an FDIC insured bank.

After years of problem solving and overcoming what I thought were insurmountable obstacles… Qube proved me wrong, and changed the face of budgeting forever.

While their unique system of digital cash envelopes straight in your bank can help even the most experienced budgeter save time on tracking (I use Qube now too)… where this really excels is in helping people who live paycheck to paycheck and are either…

- Extremely overwhelmed with budgeting and getting started.

- Unable to stick to a budget they set.

Because Qube is a digital cash envelope system that’s just as effective as an actual cash envelope system but without any of the issues that can make cash budgeting unrealistic long term (like not being able to shop online, order groceries for pick up, easily have your spouse make purchases fo you, and having to juggle cash with crying kids in a check out line), this is hands down my number one recommendation for tracking your budget and it’s the only budgeting program you should use if you live paycheck to paycheck.

Qube Money is best if you’re living paycheck to paycheck.

We’ll spend today going step by step through how to use Qube Money. I love Qube because it’s so easy to use and because it saves me so much time. Surprisingly, it’s cheaper than other budgeting options, you can use up to 10 Qubes (digital cash envelopes) for free, or you can upgrade to a partner account for $8/month.

This option unlocks partner permissions, and 2 debit cards per account or you can upgrade to a family plan and get up to 10 debit cards, and access to chore charts and kids accounts with allowances (similar to Greenlight accounts, our kids have had their own debit cards and bank accounts since they were 6).

Today, I’ll walk you step by step through how I used Qube to set up a budget and stay under that budget every single month.

Who should be using Qube?

Everyone can use Qube. It’s pretty ingenious, but you should absolutely be using Qube Money if you live paycheck to paycheck. There is no other budgeting program that I would recommend to anyone that lives paycheck to paycheck. Paycheck to paycheck means that you don’t have $1,000 in savings. It means that if something unexpected happens, you could overdraw your bank account.

The problem with traditional budgets is that they look at your month as a whole. You’re going to make $5,000, spend $4,000 on bills and pay off debt with the other $1000. That sounds easy until you attempt to pay your bills and pay off debt on the 1st of the month and $2,500 of that income doesn’t come in until the 15th of the month. Then you’re going to be overdrawing your account, racking up fees, and living off of credit cards until that mess gets cleaned up.

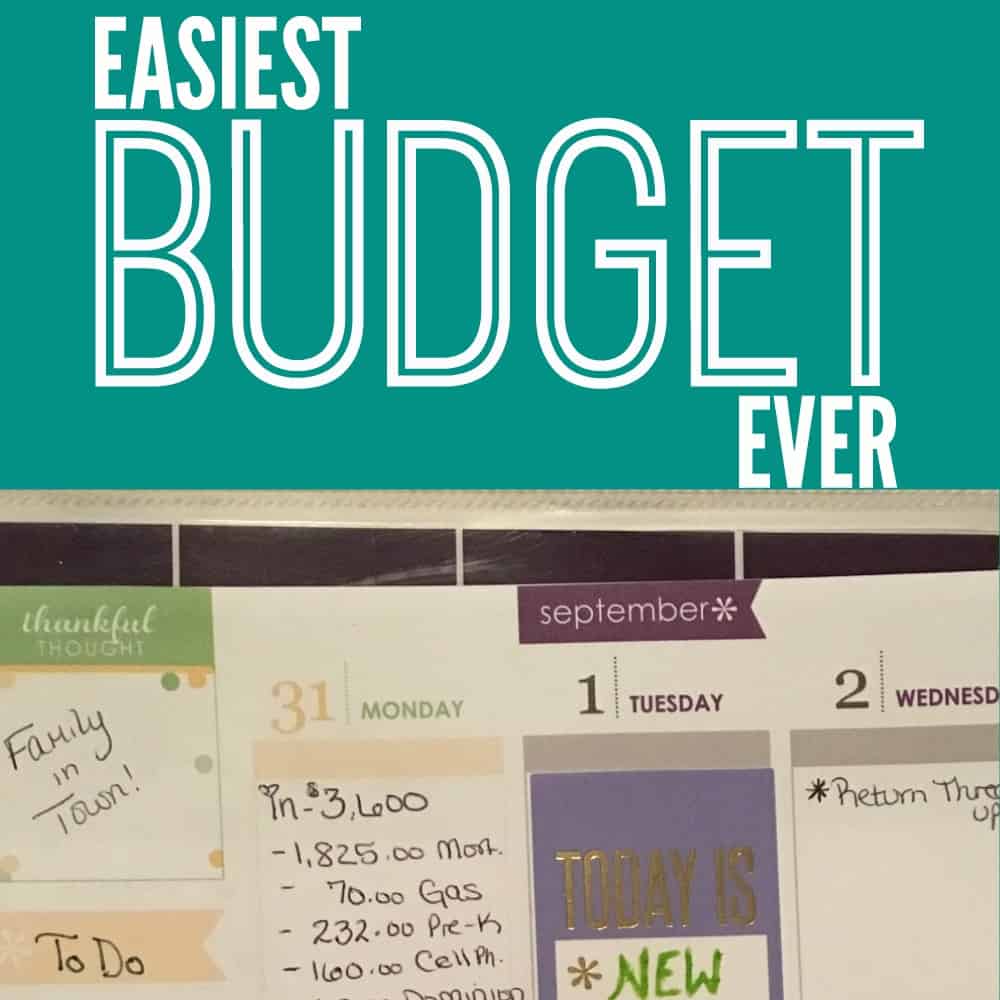

If you live paycheck to paycheck, you MUST know when money is coming in and when money is going out, and not just bills! You have to know when you need to buy a birthday present for an upcoming party, when you need money to meet your parents for dinner, or when you need to buy your Christmas tree.

You need to grab a monthly calendar and write down the dates you expect money to be coming in, and money to be going out.

Qube Money lets you assign your money to different Qubes (digital cash envelopes) so that you can immediately see what’s been funded for the month and what needs to be funded from the next paycheck.

So, now you can create Qubes (or digital cash envelopes) that match the money that needs to be reserved this month, both for normal bills, like electric and special things like “Scott’s wedding” or “dental work”.

Step by step instructions to manage your budget with Qube if you live paycheck to paycheck.

Step 1: Create an Account:

Sign up for an account here. It’s free and they’ll automatically send you a debit card. Once the debit card arrives, transfer money in from your current bank account for the month.

Step 2: Transfer your money in:

You can transfer your money in instantly via debit card. It’s limited to a one-time use on the free version but you’ll be able to use it as many times as you want with premium. The limit right now is also $100 but that’s really only going to benefit someone who uses Qube just for their fun money.

They also have direct deposit and Payday 2 Days Early which are the quickest and easiest way to get money into Qube (more on that as I test them out).

A better way to do it is to link your main bank account to Qube Money so you can transfer money from your main bank account to Qube. Those transfers take 1-3 days but don’t have limits on how much you can transfer in.

When the money is transferred in, it’s transferred to the cloud. You can’t spend that money until…

- It’s transferred to a Qube.

- You open the Qube for spending.

Step 3: Create Budget Categories:

Let’s say, on the 1st of the month, you get your first paycheck. You set up the following envelopes: (Hint: You only have to set up envelopes once but you can change them, delete them, or add more at any time)

When you set up envelopes for bills, add in the amount typically due right on the Qube name. So if you pay $88/month for your cell phone bill, write “TMobile $88.”

When you label the food Qube, write down the amount you have to spend on food every week (so take your monthly food budget and divide it by the number of weeks in the month) and choose a day of the week for you to release next week’s food budget to yourself. (I do mine on Sundays).

- Mortgage

- Electric

- Cell Phone

- Internet

- Food

- Babysitting

- Date Nights

- Transfer to Savings

Make sure to include envelopes for items that are just occurring this month; things like…

- “Tennessee wedding”

- “Dental work”

- “Jon’s Birthday”

Take your income and start transferring money to your Qubes starting with the most important ones due in this paycheck and then moving on to optional Qubes.

(So mortgage due on the first gets paid before electric which is due on the 17th because it’s more important, but it’s also funded before “Jon’s birthday party” because that’s not a “need” (although Jon may have a different viewpoint on that).

Then create an additional Envelope called *** Food Holding***

This is the account that will “hold” our food money when we get paid, and then we’ll release a weekly amount that can be spent that week into the food Qube.

The reason that we do that is if we get $800 a month for food, but we spend $500 in the first week, there’s no way we’re going to be able to stick to that budget. We need to release money weekly.

Then, create an additional envelope called “blow money” or “fun money.” Every time you are under budget in any category at the end of the week, take 20% of whatever money is left over and transfer it to your blow money account. You can spend this guilt free on whatever you want.

Take the remaining 80% left over and transfer it to the savings Qube. You can either pay off additional debt with this money right away, or you can transfer this money to a hard to reach savings account (where you keep your emergency fund) like Capital One 360 or Ally Bank.

Step 4: Spend Money

Now you’re loaded and ready to start spending!

When you go to make a purchase, whether online or in person open the Qube app first, choose which envelope you want to spend from, and open that Qube, like this…

The money available in that Qube will be loaded to your Qube debit card for the next 30 minutes or until a transaction is processed. When you make a purchase (or when 30 minutes times out with no purchase) then whatever you didn’t spend goes back to that Qube category.

Just like actual cash envelopes, you get the benefits of forcing yourself to look at your accounts and make decisions about where that money will come from before every purchase.

This is a super simple shift from a normal budgeting app, but it’s also the secret behind its success, especially in those that struggle with traditional budgeting.

Step 5: Close out the week

At the end of the week (or whatever day you reset your budget, we do it on Sundays)…

Go into each category that should have been spent to zero that week (like your food budget) or a special event like Jon’s birthday and take 20% of the amount you have leftover from the week and transfer it to blow money. You can now spend that guilt-free on whatever you’d like.

Need help calculating percentages? Use percentcalculator.net to make it easy.

Then take the other 80% of what’s left and transfer it to savings or to pay off extra debt.

Have a quick budget meeting about how you did budgeting this week. This meeting can be 5 minutes tops. You can look at your Qube balances, make any changes that are needed, and brainstorm ideas for things that didn’t work.

Advanced: You can also choose one way to save money every single week and implement it over that week. This could be as simple as calling around for competitor’s quotes on car insurance or as quick as scrolling through your iPhone subscriptions (which can be found here) and mass canceling them all).

Get Your Next Paycheck:

When you get your next paycheck. Do the same thing again. Transfer your money in, distribute it to the rest of the Qubes until they’re all full then continue spending.

Hint: If you frequently end up with last-minute “emergencies” that break your budget (which is common when you’re just starting because you’re forgetting about things frequently), create an “Oops” Qube with a smaller amount in it (between $50 and $200) to cover mistakes that pop up (like when you forget about a quarterly bill or an important event that requires money).

Use savings to live on last month’s income (an automatic emergency fund).

As you do this successfully for the next few months, I want you to keep in mind that your goal should be to be in a place to live on last month’s income. Then your paychecks for the current month will get deposited into Qube’s cloud and just wait there until the first of the month when you can fill the Qubes all at once (make sure though that you release month-long envelopes like discretionary and food into weekly allotments so you don’t spend it all at the beginning of the month and run out of money before the end.

It makes budgeting even easier. Fill your Qubes at the beginning of the month. Check them every week and transfer any weekly left over to blow money accounts, and that’s it. You can spend extra time and effort on reducing your expenses, but the bare minimum is done in just that time.

Closeout the month:

At the end of the month, check other available accounts to determine if you had “unauthorized spending” and if you did add that to the amount you budgeted for at the beginning of the month for your total spending.

If you want to go the extra mile, you can quickly categorize all your purchases into 5 simple budget categories to determine total spending by categories that you can compare month to month. (I do this every month).

But if you get overwhelmed and don’t get to that, it’s not the end of the word as long as you use the digital cash envelopes and incentivized savings to reduce spending and stick to your budget.

Then set up your monthly budget for the next month.

Warning: This is an extremely effective way to budget. It’s arguably the EASIEST And MOST EFFECTIVE way to budget available today. But it has one drawback.

If something happens to your phone… it dies, you don’t have service, or it shatters and you can’t use the screen, etc. You won’t be able to open a Qube and your debit card won’t work. There isn’t a way to bypass needing to open the Qube.

How to work around that is to keep a backup payment method in your wallet that is not a credit card. The easiest way to do this is to keep the debit card for your main checking account (whatever you use now before you have Qube) with a $50 or $100 balance in your wallet.

If you’re traveling and know that you won’t have service for the next few hours or days, you have the option of opening a Qube for an extended period of time like a few days or a week.

If you’re traveling internationally, the Qube card has been shown to work. I would have an alternate method of payment so you are always prepared.

In my case, I have a business debit card and I just keep that in my wallet in case that happens. I can use it and then transfer the money over after.

But it’s never actually happened and I haven’t needed to do that.

It’s important to remember that while this is insanely powerful technology, in order to benefit from that, you have to accept that you may one day be in a condition where it’s not possible to use it.

This system of digital cash envelopes is the single best tool to get you out of the “panic mode” with money.

Living paycheck to paycheck is a serious issue. I don’t need to tell you that. You know that. You live with that stress every single day.

You have the tools to change this now.

I can’t make you sit down and do this. But whether you read this and think “I should do that” and never actually do or you sit down tonight and actually implement this system is up to you.

You are the only person with the power to change your financial future.

Choose wisely.

You can do this. I can help.

You can join the (also free!) 90-day budget boot camp and I’ll tell you exactly what you need to do in step by step simple instructions to get your finances under control. This program has changed the lives of over 65,000 people (many of whom have been trying and failing to get their money under control for years). Take a breath… We got this. 🙂

Join the budget boot camp here.

Update: 05/15/18 You can now join the 90 Day Budget Boot Camp for free! Get step by step instructions for how to set up a budget, maintain a budget, and save money. With hundreds of success stories and reviews, this is not an opportunity you want to miss! Join the Budget Boot Camp here.

What’s the worst thing about living paycheck to paycheck?

Other popular articles…

How To Find the Best Budget App to Track Your Budget.

How 14 Bank Accounts Saved Our Budget.

Banking services for Qube Money are provided through Choice Financial Group, Member FDIC. Qube Money is a financial technology company, not a bank. The Qube Money Card is issued by Choice Financial Group, Member FDIC, pursuant to a license from Visa

This post may contain affiliate links. If you click & make a purchase, I receive a small commission that helps keep the Busy Budgeter up and running. Read my full disclosure policy here disclosure policy here.

Great site! Wish I had found this a long time ago. I am a disabled Veteran and a senior citizen on a fixed income. This site has so much good information for those of us who are not afraid of computers and modern conveniences. In plan to make the most out of the information here. Thanks a bunch. Tom

I’m so glad to help Tom! And thank you for both your service and sacrifice!

I’m new to your blog and I feel like you’ve saved my sanity!! I’m a young mom of a 2 yr old and pregnant with Baby #2 who should be here any minute.. Money has a problem in our marriage from Day One and the calendar budget is the first time I feel we’ve been able to find a middle ground on a system that makes sense to both of us. I now feel hopeful that we’ll be able to pick ourselves up from the mess we’ve gotten ourselves into.. I’d love to see an article on the different categories to budget for and things that are usually forgotten.. I’ve set up this month’s categories based on the expenses we’ve had so far but I’d love to get ideas on things that are usually forgotten!

Thanks again for bringing this topic into our lives!

I’m so glad we found each other then! And I’m a step ahead of you! I already made you one! https://www.busybudgeter.com/a-sample-budget-to-help-you-create-your-own-budget/

I am a 53 yr old woman who has been on her own for four years now. I make a very good salary but find that I don’t seem to have enough money each month. I have been beating myself up for how poorly I manage my finances. I have been very worried about my future. Today was my lucky day, finding You!! At this moment I feel there might be hope for me! Thank you so much for sharing this information! I really hope I can do this!! #feelingpositivenewbeginnings

I loved this Anne! You can totally do this! Financial security will change your entire outlook!

I have been doing something similar, using a Word document but this is going to make it so much easier!! Thanks for the share. When we started this, it really informed our spending habits. Hopefully, the calendar will help us cut even more on spending.

Just signed up for Calendar Budget. Thanks so much!!! I’ve been looking for a free budgeting system 🙂

Love Calendar Budget… I should get them to pay me as their PR person, haha.

I just started my free trail, but I have a question. Where do you put the PROJ? IT sounds like it should be in the money amount, but when I do that it says what I have put is invalid. Maybe I am misunderstanding what you wrote above.

Thanks

Yep! The PROJ!!!!! is actually in the description (where “WELLS FARGO< CAR PAYMENT" would usually go). When you transfer your actual bank charges in, you don't want double reporting, so I do this so I can easily find them and merge this entry with the entry from the bank.

I’ve been using YNAB for 4 years and LOVE it, but just now found through your site the calendar budget and one thing I use for so much at home and work is loving to see my calendar at a glance, but never could figure out or find a program that did that, so I am thinking of using it along with YNAB to see how it helps. Do you still use calendar budget? Love your blog, thankful I found it, and I don’t even know how I came across it but here I am! 🙂

I’m thrilled you found me Kim! I do still use it! I switched to Ever Dollar because they autoconnect with your bank, but then it stopped working with USAA so I’m back to calendar budget. 🙂

I started my paper budget Jan 2016 and can’t wait to get comfortable to download calendar budget!! My problem has always been buying on sale and not realizing things go on sale again! Retraining myself if I don’t need it don’t buy it!!

Mint by Intuit = Best budgeting tool ever that I’ve had! Links any and every account you have and automatically updates them. Plus, It’s FREE! The website has more tools to add more categories for budgets & the app is great too.

Every Dollar is free (I use it & don’t pay for it…)

I use ready for zero. You connect all of your debt accounts into it and it tells you how to pay them all off. Being that my biggest debt is student loans, this app is amazing, and free. It also allows you to manually enter bills that you have due and adjusts you budget.

I also use 52 weeks. Which is a savings app. You program in how much you want to save and it divides it up over the year and you just put that much away every week to meet the goal. What I’ve been doing it entering the amounts of my student loans and saving that money up. I’ve been paying off the little loans for now. (Makes me feel accomplished) now I’m working on the higher interests accruing loans. I’m still in deferment for 20 months. I’m hoping I can make a small dent.

If you can make payments while loans are in deferment, definitley do so. They will apply to your Principal balance, and not just get eaten up by interest. If you can find a way to save some, as well at a decent interest rate, at the same time, even better. And if you qualify for loan forgiveness, or can reduce or eliminate those loans via any of the programs offered through the Dept of Education, do so. There are several options, so don’t hesitate to ask.

Reduce Stress with Budgeting Apps, Software or Services Creating a budget and sticking to it can lower your debt and erase stress, making you a happier and healthier person- I use Geltbox money -automatic download from any website (banks,credit cards).

I like that I can keep my data locally instead of in the cloud.

An excellent home finance planner and tracker.

I’m so glad I found this Rosemarie, thanks! I’ve always been reading your blogging stuff and only recent got into your posts on saving money and budgeting. So helpful!

We get paid weekly, looking for maybe an envelope type desktop program. Will this calendar work like that?

I was excited about trying Calendar Budget. I had already tried both EveryDollar and YNAB and didn’t like either one. I was disappointed that the budget amounts in Calendar Budget are still monthly, and I can’t figure out an easy way to see how much I have set aside for groceries or gasoline until the next payday. I also don’t like that it doesn’t link up with my bank to import my transactions like the others do. I’ll keep looking for now. My spreadsheet works. I just get frustrated having to go through all of my bank transactions over and over because the bank doesn’t have a way for me to check that I have recorded a transaction and the order of the transactions changes, so every time I try to update my spreadsheet, I have to go through old transactions and figure out where I am all over again.

The last two years have brought on so many challenges. My husband and I worked at the same employer and they let us go right after having our second child due to conflict of interests. Needless to say, it was a shock since it wasn’t an issue before I went on maternity leave. So, fast forward to 2017 and I’ve been a stay at home mom and my husband worked full time. We didn’t have a budget and have had so many issues with his job changing his income to commission and shortening his pay and working longer.

So, he changed jobs…it’s less income, but consistent amd we know finally what we will get each pay period. To top it all off, we are due with a very surprise baby in July. Our third, and we are stressing over every penny and we keep going further and further in debt with property taxes and credit cards. We are just sinking and not able to breath. A time when we should be excited for a new baby, we are drowning and I feel stressed beyomd my 32 years. No savings, no ability to have a retirement, college savings for the kids. We will have three kids and no way to provide for them with the way things are going.

So, I’m going to invest in your article and start today with a serious budget. We only have about $250 to live on each month…so, I need to figure out how to get some extra in so we can buy food and gas to get my husband to work.

Thanks for reading amd I’m glad I stumbled across this article.

Oh Shelly, I’m so sorry! That’s so stressful. 🙁

Just take a deep breath and know it’s gonna be okay. Just keep swimming! And those kids of yours? No matter what you can provide right now or in the future financially, they’re going to admire you so much for how hard you’re working. And that’s a darn valuable lesson 🙂

Calendar Budget is no longer free and I’m a paycheck to paycheck struggler. Any budget sites/programs available?

I just found another one like Calendar Budget… it’s called DollarBird. Give it a try, as far as I can tell it’s free unless you want to add some premium things.

Thanks for sharing! I think planning and anticipating are a hard shift for the younger generation. Spontaneity, unless its free, doesn’t help budgeting!

It’s a nice tool but CalendarBudget is no longer free, it’s now $3.99 a month.

What to do if you are self employed and you aren’t sure when your money is coming. We usually play catch up.

Luring people to a website who are living paycheck to paycheck and then trying to sell them a budget should be a crime.

Hi Rosemarie,

It looks like Calendar Budget is not free (or no longer is free). Still pretty cheap and I love to be able to see and project on the calendar. I am a visual person!

Thanks for the great tips!

Try Cubux.net,it’s amazing

you have YNAB listed as $60 for life .. thats a far cry from the $98 a year they charge !!!!

Thanks for this Nick, apparently we need to update our info!

Your article is very good. thank you…!

shooting games that are for free

For so many years I have wanted to create a budget for our family but could not do it because of money not being there on a consistent basis. Now I am looking at being just myself, 62 with rising housing costs and wages that don’t keep up. Not to mention having to rely on credit cards for medical/dental expenses.

Hi Rosemarie,

You may want to update this page to mention that the CalendarBudget app is $3.99 a month. Sadly it appears to be no longer free.