When you’re setting up your budget, everyone uses budget categories. By switching to simple budget categories though, you may increase your chances of actually sticking to that budget that you’re setting up.

This was the case for me and thousands like me, who have tried and failed to stick to a budget their whole lives. Once I started using simple budget categories, it simplified the budget, made it easier to make adjustments as I went, but still gives all of the rewards of budgeting.

Update: 4/5/20 I know how stressful finances are right now with stay at home orders and the pandemic. I also know that I’m uniquely qualified to help you. I’ve helped hundreds of thousands of people get out of the paycheck to paycheck cycle (after trying and failing for years), by teaching them how to work with their unique personality to actually stick to a budget.

I’m giving you access to the insanely popular 90 Day Budget Bootcamp for FREE. Because I know that this program will change every aspect of your life. Take a look around. Because this is the LAST DAY you will ever sit around worrying about money. Let’s get to work.

Join the 90-day Budget Bootcamp for FREE here…

Fair warning though, I don’t want to give you the impression that switching to simple budget categories will fix all of your issues if you’ve never really been able to stick to a budget. Weirdly enough, it’s usually people’s home management routines that have the biggest impact.

Which kind of makes sense. I mean the two biggest budget busters are impulse purchases and grocery spending.

So when we teach people the simplified hacks to automate all their errands and to realistically menu plan for hectic schedules…

Without trying their spending goes down considerably (and they save money).

But even if you’re not at the point where you’re serious enough to try that, switching to simple budget categories is a big time saver and it makes it easier to budget.

I love using simple budget categories because it’s basically halving the work of using a typical budget, but you get the same results. In many cases, you get better results. Why? Because it can be really overwhelming to budget the traditional way.

Here, let me explain…

The Most Popular Budget Methods

Let’s start with the two typical but more complicated budget categories that people use:

The first is the Dave Ramsey Method:

He lays out categories and then suggested percentages for each.

Giving: 10%

Saving 10%

Food 10-15%

Utilities 5-10%

Housing 25%

Transportation 10%

Health 5-10%

Insurance 10-25%

Recreation 5-10%

Personal Spending 5-10%

Miscellaneous 5-10%

The second is the “Specific Method.”

This is what people usually come up with when they do their own budget categories. They may use the Dave Ramsey Percentages above as a “goal” for making decisions like what house to buy, or how much to save, but they base their budget on the bills that they currently have.

They list every bill they have and the exact amount…

Mortgage: $1,200

Cell Phone: $80

Electric: $240

Vehicle Loan #1: $150

Vehicle Loan #2: $180

Credit Card #1: $140

Water Bill: $45

Trash Service: $20

Day Care: $688

TV/Internet: $66

Then they assign reasonable amounts for everything else:

Savings/extra debt pay off: $400

Food: $700

Fuel: $200

Clothing: $50

Vacations: $50

Haircuts: $40

Kids activities/sports: $80

*If they’re really game on, then they’re setting up budget categories like clothing and vacations as funds, so it can accumulate that monthly income and build up over time.

If you’ve budgeted before and stuck with it… then you’ll likely want to stick with traditional budget categories (I mean, why fix it if it isn’t broke, right?)

You can get a refresher on how to budget right here if you need it…

But… If you’ve tried to budget dozens of times before and haven’t ever actually stuck with it… then you can toss those out the window and switch to Simple Budget Categories.

Simple Budget Categories

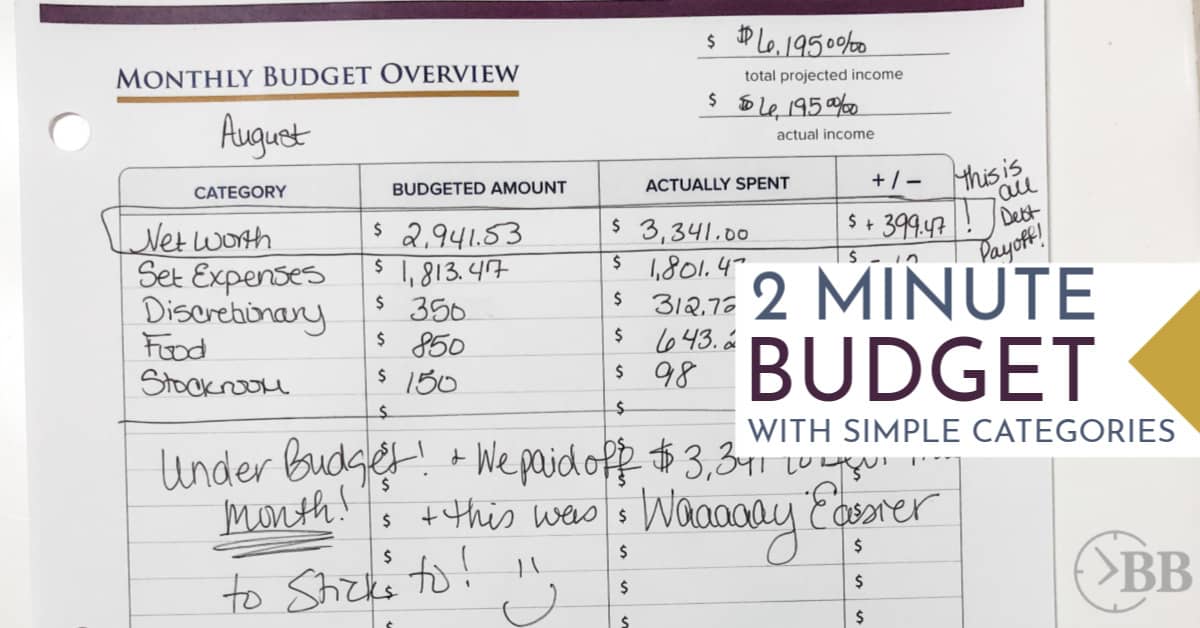

When you use simple budget categories, everything you spend fits into one of five categories.

Net Worth

This includes your mortgage, car loans, credit cards, savings accounts, retirement, or investments.

Basically, anything that has a positive effect on your net worth when paid into.

Set Expenses

These are things that you aren’t making decisions to purchase, they’re just set up as monthly purchases. Things like rent, taxes, insurance, internet, electric bills, etc.

We also put fuel and medical expenses in here as well, since few people make the decision to overspend on fuel or medical expenses.

For the most part, these aren’t impulsive purchases, they’re set up ahead of time (but you can still reduce your spending on these!).

Food

This is the single biggest area of overspending. It includes groceries, eating out, and school lunches for kids. Basically, if you put it in your mouth and it travels to your stomach, count it here.

Stockroom

This is all of the stuff you need to run your home, from toilet paper to deodorant and air filters. If you’ve automated this fully and you know the set monthly amount you spend on this, you can add this to your set expenses and eliminate this category.

Discretionary

This is everything else. Things like personal spending, outings, date nights, home goods, new shoes, hair cuts, vacation, goals, fun and even things you didn’t plan for.

Almost all overspending comes from just two categories… Food and discretionary.

While it’s absolutely possible to reduce the spending across each of the categories, you’re going to find the biggest savings in those two categories.

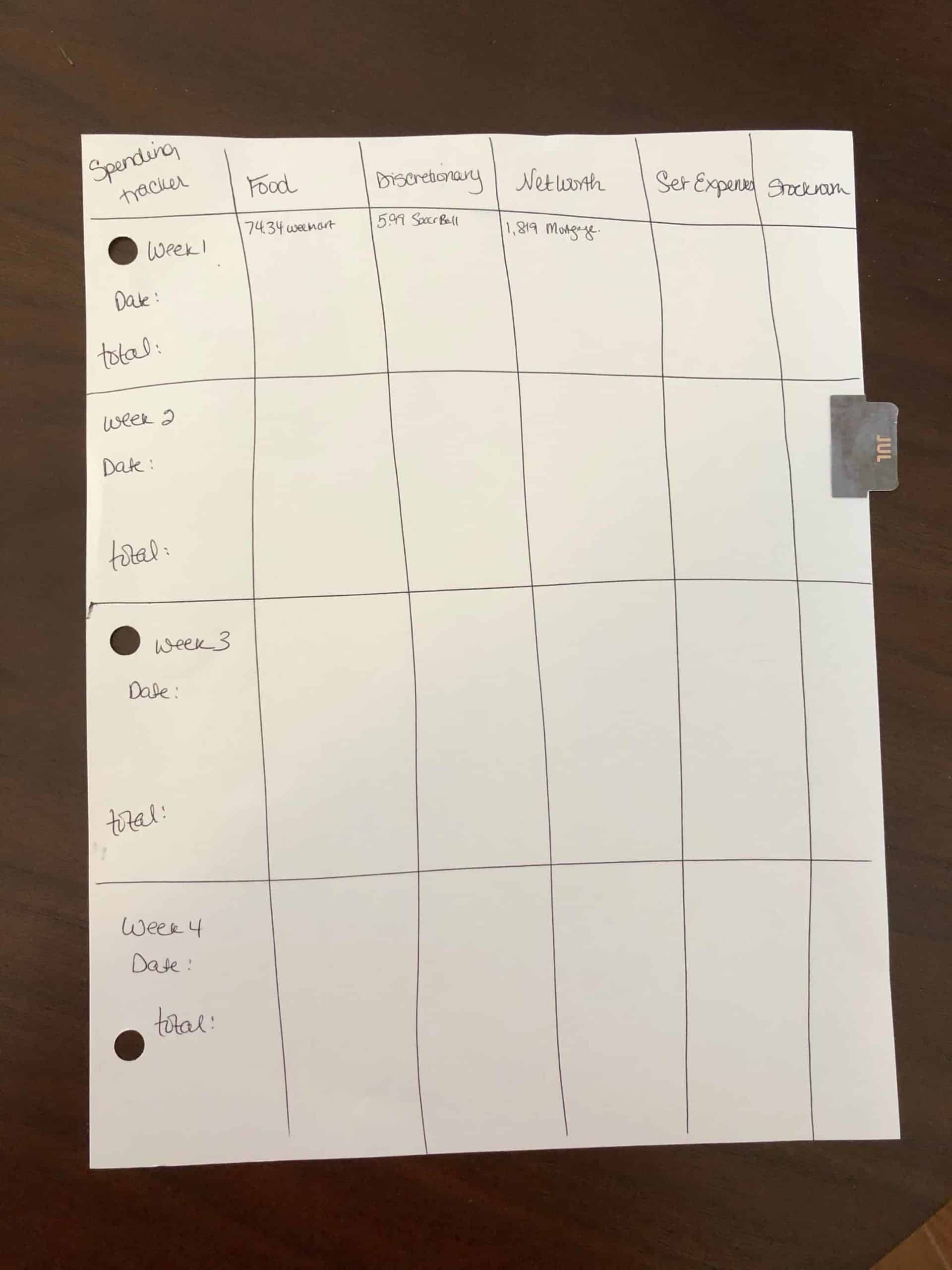

Daily Tracking: Because you only have 5 categories to worry about, it’s easy to track your spending every day. You can use the daily spending tracker in the easy budget binder or just draw 5 columns on a piece of paper with 4 or 5 rows (like below).

Each day, just list what you spent yesterday on the daily tracker. It takes literally seconds to minutes. You can load banking apps right on your phone while you sit down for breakfast. (No time for breakfast? That’s where those home routines come into place).

Each month, try to spend less than you spent last month. Any extra money left over after you reduce your spending, goes to your Net Worth category (like your debt or savings), but keep at least 20% to incentivize your savings.

This means… when you reduce your grocery spending from $1,200 a month to $650… You saved $550 that month, so $440 is going to either an extra debt payment or your savings or investments, and $110 is going to whatever you want most in the world (hint: These are my favorite things to buy).

Using the simple budget categories Stockroom and Set Expenses rarely change. They just kind of go on autopilot (especially if you use the simple stockroom method to run your home on autopilot for less money).

That lets you put all of your focus on the discretionary and food categories. Food is usually the largest category to reduce (but can be the hardest unless you go through the steps of simple meal planning for beginners).

If you’ve always sucked at budgeting and have never been able to stick to it, then switching to these simple budgeting categories and tracking it every day will do the trick (especially if you’re incentivizing to spend less than you did last month!).

If you’ve tried this and can’t believe how easy it was to stick to… get on the waiting list for Hot Mess to Home Success.

It almost always has a waiting list, but it teaches you how to work with your unique personality to master every level of home management (budgeting, meal planning, cleaning, decluttering and automation) so that you NEVER have to deal with a trashed house and money fights again.

And, it teaches you how to use bare minimum consistent effort to master home management and budgeting.

Fun fact: Hot Mess to Home Success started as a budgeting class for people who could never stick to a budget. They were the people that would sit down and make a budget and swear they were going to stick to it… but in a few days to a few weeks, they’d be right back to where they started.

What they didn’t understand is that your home (and life) routines HAVE to support your ability to save money. When we started sending beta testers through the budgeting program, they were sticking to a budget and paying off debt but they were FLOORED by how they got (and kept) they’re house clean and got (and stayed) organized almost immediately.

Because without that minimal consistent effort to get your life under control, your budget relies on will power for you to stick to it (and realistically, that’s not going to happen).

So, Hot Mess to Home Success got ‘internet famous’ for teaching people how to get and stay organized and manage their homes well, particularly if they’ve been trying and failing to do that for years… but the end result is that you always set and maintain a budget easily… without needing willpower to stick to it.

You can get on the waiting list for Hot Mess to Home Success here, and they’ll send you their starter program for free (so you’re ready for the program when you can get in).

P.S. Overwhelmed on how to get started? You can get the Easy Budget Binder for just $9 today. It gives you step by step directions on how to set it up and maintain your budget, and it has built in incentivization so you actually stick to it. Plus, it’s so easy that you can do it in just two minutes a day. See Cara’s walkthrough of how she’s using the Easy Budget Binder to pay off over $100,000 in debt as someone who self admittedly used to suck at budgeting here.

P.P.S. Budgeting isn’t really something that you learn to do overnight… And if you suck at budgeting, it can be hard to “fail” while you figure it out (because overdraft fees are expensive!). If you suck at budgeting, there’s a pretty easy hack to stop overdrafting your account while you get better at budgeting. We recommend that everyone do this… I made you a video to explain how.

We have used what you call the Specific Method for quite some time and I feel that it works best for us that way. Since amounts on many important bills change on a month-to-month basis, we feel like we can better manage our money if we write down the exact amount of income and the exact amount that will be going to each category. That way we also decide what gets paid with which paycheck, depending on each bill’s due date.

We also use budget categories to keep a clear picture of how much of our money goes where. And we revisit the budget frequently. That is the only way to make sure it’s current and fully functional 🙂

Neat to see different budget categories and compare. Thanks! Counterintuitively, we start with some of the FUN categories first (like entertainment, theater, arts, etc) and proactively estimate what we want to spend to have fun in the areas we want to. I know this as Conscious Spending, I think Ramit Sethi coined that one. Have you looked at incorporating something like this before?