If you have no idea how to budget, or worse… you can’t ever seem to make yourself stick to the budget that you set… then the Easy Budget Binder is the easiest way to get started and to stick with it because it’s build from the ground up to work with your unique personality. Even if you don’t have will power or are super impulsive.

This was the secret to reducing our spending by over $23,000 a year, paying off our debt of over $30,000 and finally understanding budgeting after 12 years of trying and failing.

If you don’t already have The Easy Budget Binder… you can get a copy here.

If you do have it already and want someone to walk you through exactly what to do, step by step… you’re in the right place. I’m going to walk you through how we successfully fixed Cara’s financial mess with The Easy Budget Binder.

This all started when I got an email from Cara that said…

“I have no idea how much we owe but I know it’s around 100k. It feels like we’ve been trying to get better at budgeting for years but something always happens… the roof needs to be repaired, a kid needs braces, or we forgot something and overdrew our account.”

We have four teenagers and I think we’ve really given up any hope that this will ever be fixed. I’ve tried every budgeting printable and program I could find and we never stick with it for more than a week or two.”

“If I’m being honest (and I want to be) I don’t think either of us thinks it’s possible to fix this.”

Too much debt to fix?

“We do what we need to do to make it through the month and try not to think about the future.

But when I heard your talk about budgeting and how you focus on the most severe cases… I thought this might be worth a shot. Because I don’t really know what else to do.”

We asked her if I could share her email and the photos from her Easy Budget Binder in exchange for getting her started.

And she happily agreed.

Start where you are.

I wanted to do this because while many of you are in a better situation than Cara… a lot of you aren’t.

A lot of you look at Cara’s situation with complete understanding… you get it.

And when you read “budget advice” where they have 2 credit cards and high incomes, it makes you feel like this will never work for you. I get that.

I’ll walk you through how Cara got started using the Easy Budget Binder, so you can do the same.

If you don’t already have it… you can get the Easy Budget Binder here at 66% off.

But the thing is…

This WILL work for you. I don’t care how bad off you are right now. Or how many bad decisions you’ve made… this is fixable. This is ALWAYS FIXABLE.

The Easy Budget Binder is your best chance to get this under control…

The Easy Budget Binder (printed half size to fit a mini binder) nestled into a budget box which has bills, checks, pens, envelopes, and stamps.

Fair warning though, while the budget system we use is easy and only takes two minutes a day to maintain, this post is long. I wanted to make a super detailed step by step walkthrough of how to do this with someone with a ton of debt. If you just need the highlights, we have more condensed instructions for you in the Easy Budget Binder and then you can always come back to this if you’d rather see a real life example.

Own your mess.

Don’t apologize for who you are or what you’ve done. If you’re impulsive and don’t have a ton of willpower… that’s not going to change. Any plan that assumes you won’t act impulsively or you’ll suddenly develop willpower is guaranteed to fail.

We always work with the personality you have to implement changes that will work naturally, without force.

Look at your numbers clinically, with no thoughts of failure or emotions. It is what it is. Don’t feel bad about the choices you made and don’t dwell on them. Accept them and move on knowing that from now on, you’re working with your personality and you’re in a better place now.

Tell kids that you’re budgeting.

Tell older kids what’s going on.

With Cara’s four teens (and pretty constant requests for money), you’re going to need to bring them into the fold.

You’re teaching them about money when you ignore it and you’re teaching them about money when you tackle it. Which lesson do you want them to have as they grow up?

Important: you don’t want to terrify kids with details. You can simply say “We’re saving up for an epic retirement and want to get better with money. We’re focusing on that right now. We decided we want to be debt-free.”

Tackle basic home management first.

Cara describes herself as a hot mess. Her laundry’s behind. Her sinks always overflowing and she always feels like her life is out of control. She can write down her budget today, but she needs to understand that it’s impossible to make headway on a budget and stick with it if you don’t have the foundation of home management under control. Because home management and your budget are related.

This is why we’ve been so successful in transforming even the toughest cases of chronic disorganization.

Because budgeting is an advanced skill.

We have to tackle automation, foundation, and meal planning first before we can ever hope to be successful at budgeting.

Building skills in the right order.

The good news?

When you learn the skills in the right order they are actually pretty easy. Because we teach you how to do the bare minimum effort on a consistent basis and never rely on your having the willpower to stick to it.

So in addition to setting up her budget binder, we had to enroll Cara in Hot Mess to Home Success, which helps her quickly learn the foundation of what she needs to know BEFORE she gets into budgeting.

As a weird little side effect, her house also gets and stays clean.

We’ve been known for budgeting for years, but we got a bit internet famous in the last two years because word spread far and wide that we can help anyone keep their house clean.

If you need the whole package (budgeting, foundation, and home management)… I’d rather you just enroll in Hot Mess to Home Success (You may need to join the waitlist first, but you’ll get the starter program for free when you do that) rather than reading this entire article and implementing all of this.

You can grab Hot Mess to Home Success here… (if it’s closed, join the waitlist and it will automatically send you the free starter program).

Then we start setting up our Easy Budget Binder…

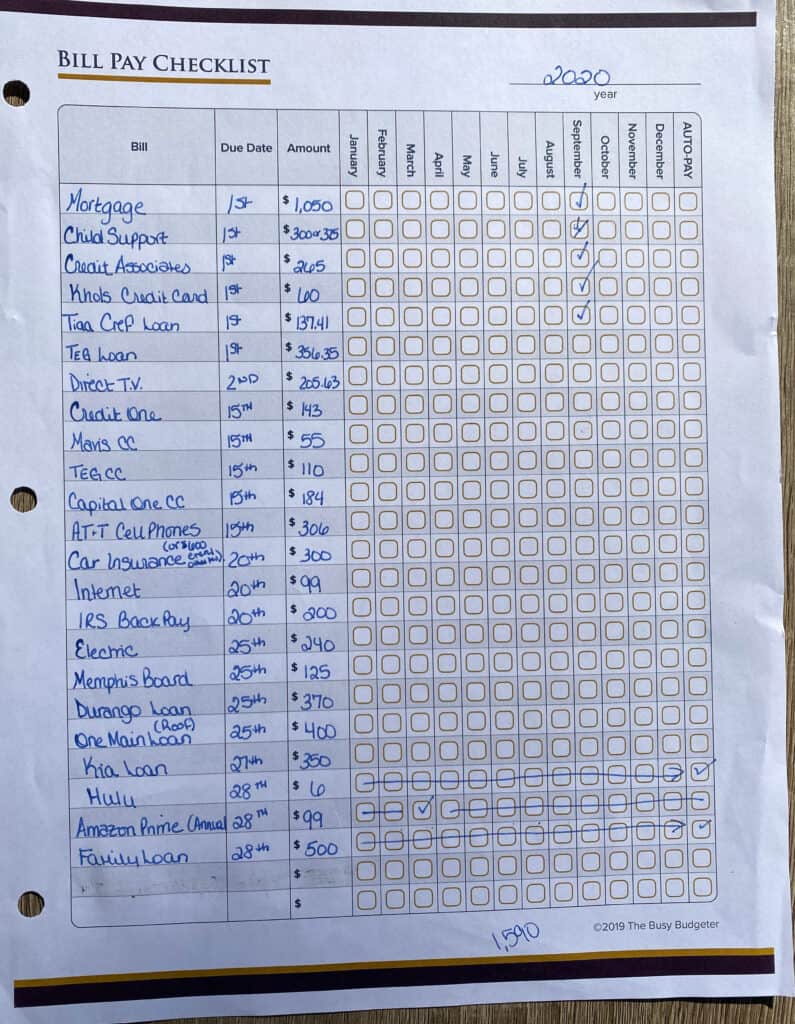

Step 1: List monthly bills on the bill pay checklist.

Why do we do this? So things don’t get missed. So we know the ACTUAL number of what we need to pay every month versus what we can remember that we need to pay. It’s not uncommon for people to find tons of subscriptions they had no idea they had subscribed to.

Bill pay checklist with checkboxes to mark off when bills are paid.

- Start with the bill pay checklist.

Anything that has to be paid every month, Hulu, your electric bill, your credit card bill go here in your budget binder. This is an easy reference for you to make sure that everyone that’s supposed to get paid, gets paid.

- First make this list on a scrap piece of paper (it will eventually go into your budget binder). So when you switch it to the Bill Pay Checklist, you can list the bills in order by the due date.

- On the scrap paper, list…

- The name of the bill.

- The due date.

- The amount.

- If you have an annual bill (like HOA dues or property taxes) cross out the monthly bubbles for all but the month that bill is due in (similar to how we did Cara’s Amazon Prime).

Step 2: Find forgotten subscriptions and auto-pays.

Hint: If you have bills set up to autopay and they don’t have the threat of back pay due if you miss it, then mark that as auto pay and cross off the whole year (like Cara did with Hulu).

What this means: If your payment for Hulu doesn’t go through, the service stops and you don’t owe anything else. You can fix it when you want to and watch it again. This way we don’t need to track that every month since it’ll get paid on its own.

But, if you forget an electric bill, your electricity might get cut off. So even if you auto pay that we don’t want to cross them all off for the year because we still need to check that.

Feel like you’re forgetting things? You are. 🙂 Almost guaranteed.

That’s why having a budget binder is so helpful.

Step 3: Track your past spending.

Before you sort the above amounts by due date and add them to the Bill Pay Checklist we need to do one more thing. Go through the last month of spending and look for things that you may have forgotten.

- You can do that by printing out your last full month (1st-31st of a month) from your bank accounts and any credit cards that you have used (don’t forget Paypal if you use it!).

Step 4: Finish the bill pay checklist.

- Once you’re done, sort your bills and add them by the due date to the Bill Pay Checklist like Cara’s.

Step 5: List all debts.

Monthly sheet to track each debt owed, amount budgeted and amount actually spent.

Why do we do this?

So we know what our total amount paid every month is to debt (over $3,000 a month in Cara’s case which is about 40% of their monthly income).

Now we understand exactly how bad things are. Then we can determine what needs to be paid first and why. And, we can see the progress of what we decide.

- Using the information from the Monthly Budget Overview, pull out any of your debts, and list them on the debt overview.

What to Include…

- Debt name.

- Interest rate.

- Minimum monthly payment (although this will change based on your balance and interest rate, it gives us a good starting point).

- Total balance right now.

For Cara, this was super overwhelming because she had no idea what most of her logins were and she didn’t have statements, so she couldn’t find a lot of that information.

I want you to do your best to get this… because it’s an essential step to fixing this.

It gets easier.

If you get overwhelmed and just never do it, we’ll never get anywhere. So do your best, and if you need to skip a few… we can come back later and fill those in to the budget binder when we’ve made a little more progress.

Hint: As Cara found her login info, I had her set up a free LastPass account, so she wouldn’t ever have to do this again. LastPass keeps all of her passwords for her (and auto-logs her info from her iPhone) so she never has to remember any of those again.

- Next, Cara calculated her total amount of debt (with and without her mortgage).

I recommend not even counting your mortgage in your debt amount right now. Just focus on the non-mortgage debt and you can decide if you want to prioritize paying off the house over investing later. (That’s a big debate with a lot of opinions but not really relevant to where you are right now… It’s kind of like you’re crayon eating kindergartener worrying about trigonometry- We’ll come back to that when we get there).

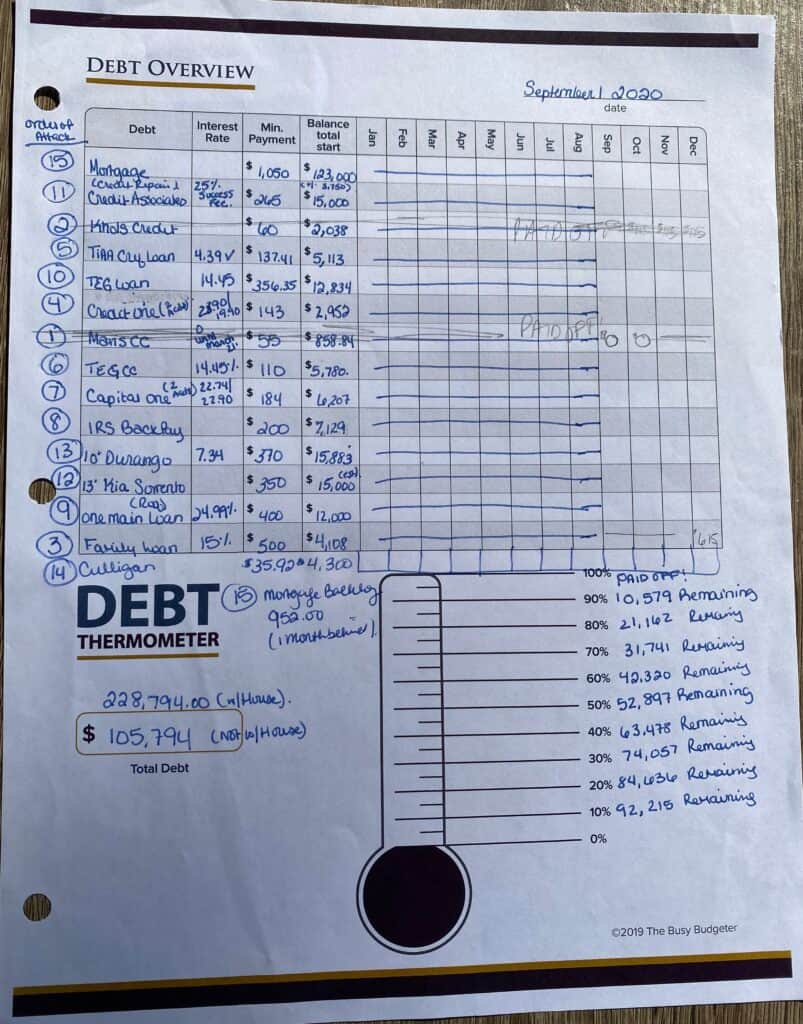

Step 6: Complete the debt thermometer.

Then we fill out the Debt Thermometer with your percentages. Now, you have a visual in your budget binder of your debt going down. (Hint: If you’d rather have a single page thermometer, without getting the binder… we have one you can get here… it’s a fridge favorite).

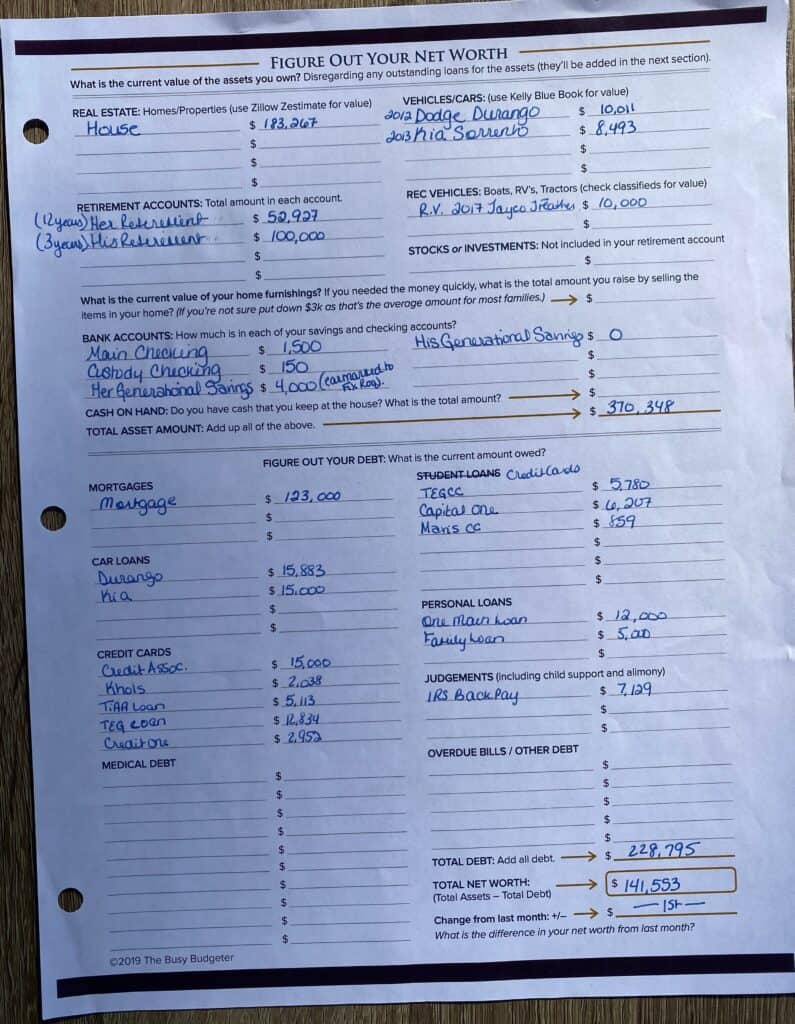

Step 7: Calculate your net worth.

Net worth worksheet to help you track assets and debt each month.

Why do we do this? This is the single best way to track your success. It’s better than tracking the debt you’ve paid off, the amount you’ve spent, or the amount you’ve saved. It’s a “big picture” view of your finances and it’s significantly more encouraging to track your net worth than the debt you’ve paid off.

- Go through and fill out the Net Worth Worksheet. Add in your assets (things you own, even if you still owe money on them).

- For real estate- use Zillow and write down the Zestimate.

- For cars- use Kelly Blue Book.

- For recreational vehicles- RV’s, boats, etc. use the price you believe you can sell it for. (I use Facebook Marketplace to estimate this by looking up similar listings).

Retirement: Cara also listed how many years they have until retirement (you don’t need to do that, that was to help me give them their budget breakdown).

Step 8: Figure out your debt.

Monthly debt tracking worksheet that includes fill in information for total debt, monthly, payment, interest rate and total balance.

- List each of the debts you owe on the Debt Overview. Compare it to your debt list. But, this list should also include medical debt, loans from family, and past due balances that are contractually owed (like if you’re one month behind on the mortgage or owe $4,000 to your custody attorney).

Judgments

A judgement is a court order that’s the decision in a lawsuit. These can be from a debt collection or from someone suing you (like from a car crash). You would know if you have any judgments, it would involve you going to court or at least talking to an attorney.

Judgments also include things like child support or alimony. You should only include child support or alimony if there is a judgment (or a backpay order). Otherwise, that counts as a monthly bill and not a debt.

For example: If you pay $100 a week for child support, that counts as a monthly bill.

But, if you have $8,000 due in a judgement or for back pay that you owe, then that’s a judgement debt.

So, Let’s say you owe an $8,000 judgment for back pay and you need to pay $100 a week of child support. Going forward you might be required to pay the $100 plus another $225 a month for the back pay.

Then you have a $100 weekly bill (which would cost $400 or $500 a month depending on how many weeks are in that month) and an $8,000 debt.

Step 9: Determine your debt payoff strategy.

If you need more lines than the sheet provides, you can attach a second sheet or just add them to the bottom like we did with Cara’s.

- Next, we determine the order of the debt that we’ll pay off first.

Typically, we pay off the smallest balances first (made famous by Dave Ramsey’s “Debt Snowball” method), this has been A/B tested to give you the fastest results.

There can be exceptions to this though…

Cara’s a perfect example of this. They had taken out a loan for $25,000 from a family member (who put it on their credit card with a 15% interest rate) with the promise to pay back $500 a month. They have paid that for a long time and have just over $4,000 left on that loan to pay back. Paying off that $4,000 first would free up an additional $500 to clear other debts faster.

Because of that massive monthly payment, we pushed that ahead of the Credit One account for $2,952, and then she’ll pay off the smallest balance first (like the Mavis credit card with $858.84 and a $55 a month payment).

When that’s paid off we’ll take the $55 a month and apply it to the Kohl’s credit card (originally, owing $2,038 with a $60 a month payment. So she’ll actually be paying $115 a month toward that now plus any additional money we can save.

Once this is established, then every month, you can use the monthly blank boxes in your budget binder to help you calculate the new payment for the next debt you’re paying off.

Here’s an example…

In September, Cara pays off the Mavis credit card, so then she adds the $55 payment to the $60 monthly amount due on the Kohl’s card and she writes $115 down in the October block for the Khol’s credit card. Hint: You can leave the blocks blank for the other debts, just use it to write down the next combined payment for the debt your working on in your budget binder.

In case this is confusing, I projected Cara out on this to show you what it will look like in December when she’s also paid off the Kohl’s card.

She marks that as paid and adds the previous monthly payment of $115 (which is $55 from the monthly payment for Mavis (which is now paid off) plus the $60 monthly payment to Kohl’s (also paid off). Then she added that to the monthly payment ($500) for the family loan as the new debt payment for December.

So her total monthly payment is $615.

The Easy Budget Binder builds in rewards to sticking to the plan.

Our budgeting program rewards Cara for being under budget by letting her keep 20% of her savings to “blow” on whatever she wants and 80% of what she’s under budget goes to pay off this extra debt.

If you’re thinking to yourself- “I can’t blow money! I’m behind on the mortgage and can’t even pay my bills!” then I get where you’re coming from but you’re wrong- and I have statistics on my side. We’ve gotten a whole lot of people who suck at budgeting to successfully stick to a budget and this is how. You can do it your way- but you’ve been trying to do it your way for years- try it my way.

Paying off your debt and digging yourself out of this hole is a MASSIVE undertaking and the “reward” is a long way away and a little vague (Do you want to be debt free in 5 years or buy Chick-fil-A tonight so you don’t have to cook?). Some people have the will power to make good decisions despite that but you don’t (if you did- you wouldn’t be reading this). In a calm moment (like when your planning out the budget) you’ll choose debt free. In a bad moment (when your on the way home with 2 kids screaming in the back seat and you just realized you forgot to thaw the meat for dinner), you’re going to choose what you want the most in that moment.

Don’t worry about the blow money or the extra debt money right now though… I’ll explain that when you need to know it. And you always have the option to skip that part and do the rest.

Bills that are behind.

Cara’s one month behind on the mortgage every month. She pays her mortgage on the last day of the month (rather than the 1st when it’s due), so that counts as a debt. Because in addition to everything else, she also needs to pay an extra mortgage payment to catch up.

You may have a similar situation with the electric or water, etc.

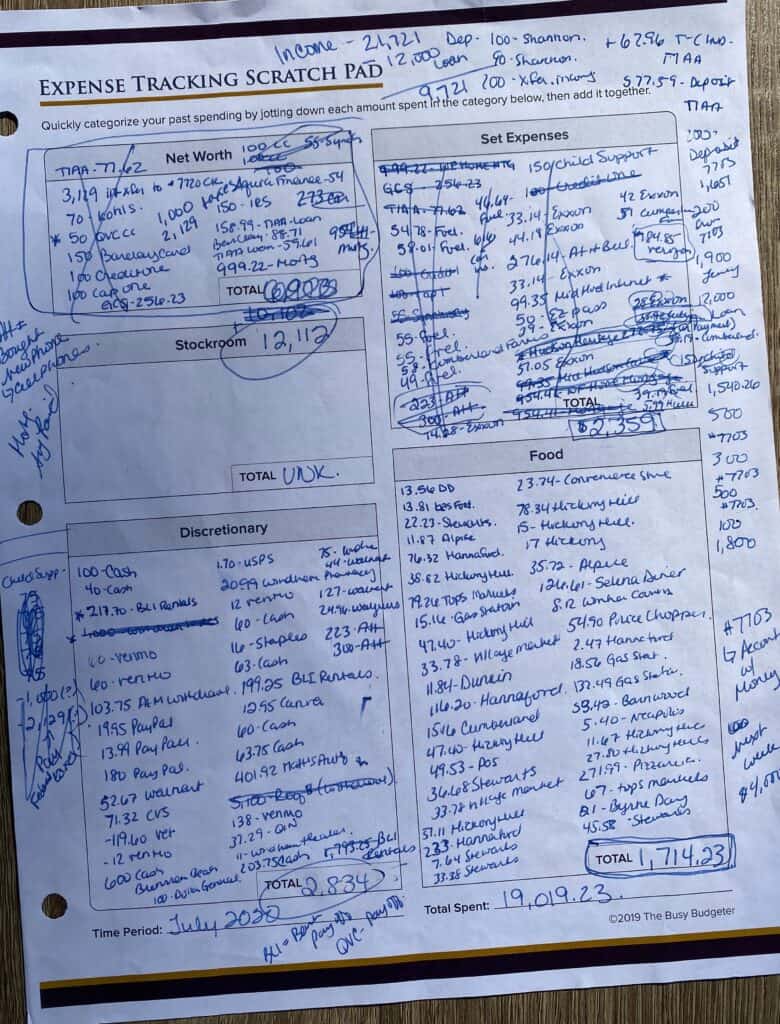

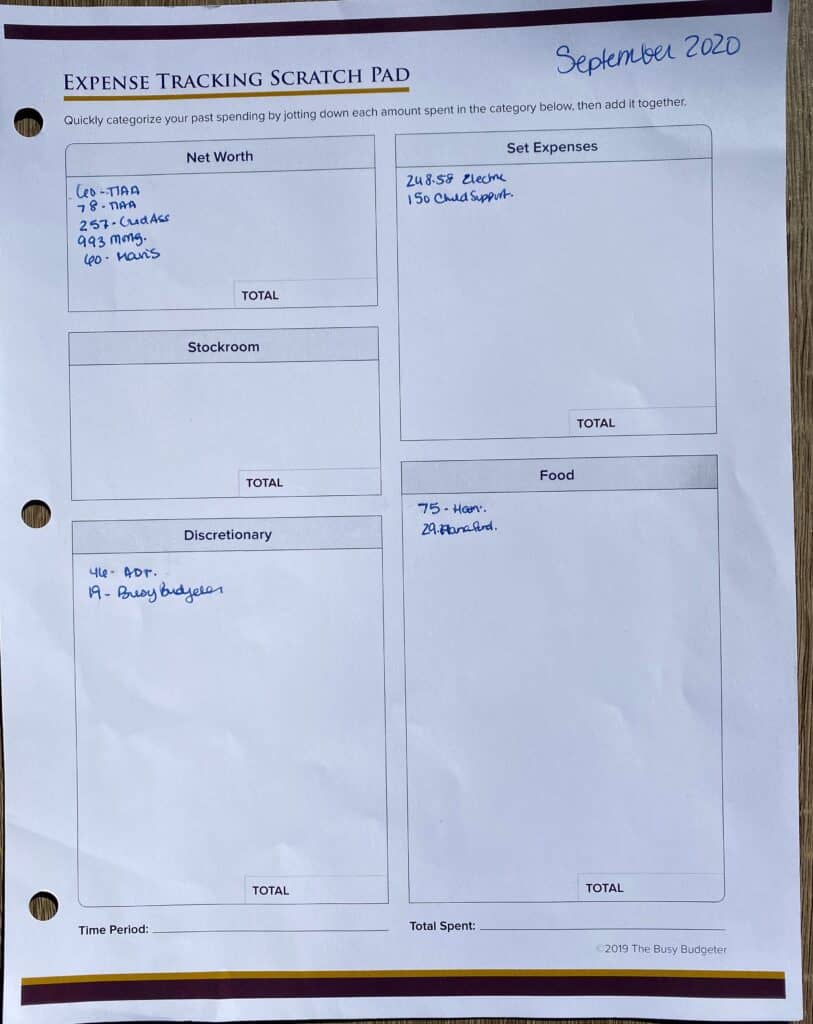

Step 10: Determine past spending.

A scratch sheet to track expenses that you have spent over the month.

Why do we do this? To find out where you’re actually starting so you can set realistic goals and judge yourself based on your own facts. This is essential because if you’ve spent $1,714 on groceries last month (like Cara did) but you don’t know that because you’ve never calculated your last month’s spending. So you assume you spent $800.

Then when you set a budget, you’re going to write down some arbitrary number that sounds right to you like $800. Now when you spend $1,300 on groceries… you’ll determine that you’re a failure and you suck at this and give up because no matter what you do… you’re hopeless.

When in fact, you reduced your grocery spending by $500 in a month which is a massive accomplishment.

The only way to be successful at this is to judge your new behavior against your past behavior. And to be better this month than last month.

To determine your past spending…

- Print off the last full one month period of any account you may have used. That includes debit cards, credit cards, PayPal, etc.

- Then grab the Expense Tracking Scratch Pad and start categorizing those items into categories. To make it easy (we teach a 2-minute budgeting system that’s amazing, and significantly easier to track than most. It teaches the 5 categories we use to track. Every purchase goes into one of those 5 categories).

Net worth.

This includes your mortgage, car loans, credit cards, savings accounts, retirement, or investments.

Basically, anything that has a positive effect on your net worth when paid into.

We want you to spend TONS of money in the Net Worth category every month. The more you spend here, the better!

Set expenses.

These are things that you aren’t making impulsive decisions to purchase, they’re just set up as monthly purchases. Things like rent, taxes, insurance, internet, electric bills, etc.

We also put fuel and medical expenses in here as well, since few people make the decision to overspend on fuel or medical expenses.

For the most part, these aren’t impulsive purchases, they’re set up ahead of time (but you can still reduce your spending on these!).

Food.

This is the single biggest area of overspending. It includes groceries, eating out, and school lunches for kids. Basically, if you put it in your mouth and it travels to your stomach, count it here.

Stockroom.

This is all of the stuff you need to run your home, from toilet paper to deodorant and air filters. If you’ve automated this fully and you know the set monthly amount you spend on this, you can add this to your set expenses and eliminate this category.

Don’t eliminate this unless it’s fully automated though (because it’s very easy to impulsively overspend in this category).

Discretionary.

This is everything else. Things like personal spending, outings, date nights, home goods, new shoes, hair cuts, vacation, fun, and even things you didn’t plan for.

Almost all overspending comes from just two categories… Food and discretionary.

- Go through your spending and write the amount under the correct category (this will look pretty messy and that’s fine, it’s a scratch pad).

- Then go through and add up the spending under each category for the month.

Often when you do this: you won’t believe the numbers are that high and you’ll think to yourself… well, that was the month we had (name some unusual circumstance here). You’re welcome to do this again for the month prior to compare the number. But, usually the numbers will be similar, there will just be a different unusual circumstance in the month before.

- Keep that original Monthly Bill Checklist around while you do this though, so you can confirm the actual amount you spent, and add in any bills you may have forgotten.

In Cara’s case: she estimated that she spent $700 a month on food, $2,000 on set expenses, $500 on discretionary, and $4,000 on net worth. For a total of $7,200 spending in a month.

While she’s new to how we budget, she had been trying to budget for years and that’s what she usually set up her budget as… she just never stuck with it.

In actuality, Cara had spent for the last 30 day period…

$12,112 in net worth. (She doesn’t make this every month- Cara had just taken out a personal loan to fix a roof and that money was included in her “income”)

$2,359 in set expenses

$1,714 in food

$2,834 in discretionary

For a total spending of $19,019 ($6,907 in categories other than net worth).

Keep in mind though, that $12,000 of that is in Net Worth (paying down debt and investing and saving) and typically Net Worth spending is good, that’s money that you’re putting towards debt or tucking into savings or investing.

These numbers would have been encouraging to me (and they were encouraging to Cara) until it was pointed out that in the prior month, Cara had her roof fail and needed to have it replaced for about $4,000. Because they didn’t have that money available, they took out a personal loan for $12,000. They set aside the $4,000 to be used on the roof and used the rest of the $8,000 to pay off other debt (not listed here because it was paid off prior to us starting).

So while it appears that she paid off 12k in debt, Cara really just moved that debt around and didn’t actually pay off any debt. Where usually she pays $4,225 to her debt every month (though that doesn’t reduce her total debt amount by that much due to interest), she actually broke even this month paying off almost exactly what she gathered in new debt.

Cara transfers those total spending numbers over to the Monthly Spending Report. She’ll do this in her budget binder every month so she can see at a glance how much she’s spent each month, and how she’s improving. She can also track how much incentive payouts she’s earned, both in her 20% blow money and the 80% goal money.

Step 11: (Optional) Create an after budget to inspire you.

What would Cara’s life look like if she didn’t have this crushing debt every month? She has no idea because she’s admittedly never stopped to ask herself what that would be like.

Visualizing that future would help her get into the frame of mind where she could create positive change. The she can add it to her budget binder so she always knows what she is working for.

While this step is optional: it’s usually fun and it can make a big difference when you see that what you’re working towards is worth the effort.

Warning: don’t fall into the trap of thinking that just being able to visualize your future is going to be enough to stick to your budget. While you’re inspired now, the fact of the matter is that when you have moments of low willpower, you’ll just want what you want at that moment and you’ll blow the budget like usual.

You need a system with rewards built in like the Easy Budget Binder to stay on track.

Eliminating the paycheck to paycheck cycle.

It’s the on/off budget cycle (similar to yoyo dieting or the trashed and untrashed cycle) that’s the problem. You’re “on budget” when you get paid and then you’re “off-budget” a few days to weeks later and you just do whatever.

When you go over budget and just do whatever you want, you get an immediate release of dopamine (the feel-good brain chemical) and new boots (or whatever struck your fancy). We need to retrain the way your brain works by having you see that the only way to get what you want (new boots and a dopamine release) is by doing what you should be doing (paying off debt and saving money).

In a perfect world, we would take 100% of what you’re under budget and put it towards your debt, getting you out of debt faster right?

But you’ve likely been trying and failing at that for years.

Because that plan requires you to have willpower.

Which you don’t have.

If you did, you wouldn’t be in this situation.

We have to get your brain to see that the reward for staying under budget is what you actually want (to blow money).

That’s the only way to get long term change in this if you can’t naturally do it.

Budgeting can actually be fun.

It also makes budgeting fun. Because it becomes it’s own little level-up game. (Budgeting and giving yourself blow money every week at your budget meeting is a huge incentive on its own to have those budget meetings.

So, give this a try.

Worst case scenario, just prove to me that it doesn’t work.

But an After Budget can help you realize that there’s another giant reward at the end of this.

You can put as much time and effort into an After Budget as you want.

Basically, an After Budget is a goal budget of where you want to end up.

In Cara’s case, she and her husband make $7,200 a month.

In her After Budget, she spends about $3,680 on bills, groceries, and funds (a separate savings account that you pay into to buy things like cars, etc. with cash (we skip the car fund and just flip cars though).

But without the almost $4,000 a month in debt payments, they’d each have $1,104 a month to spend as they want.

Plus an additional $736 a month to investments. And, $736 a month to spend on the kids (either for experiences with them, like vacations and trips, or for things they need like college help, etc.) (This is a HUGE want for them both).

Your After Budget can be as simple as saying, we wouldn’t have the 4k a month we currently pay to debt, and we could spend that however we choose.

This just helps you visualize that.

When we started, our “want” was a dream house that we could actually afford to decorate and love. I’m currently writing to you from the back patio of that dream house under the gazebo.

So, for someone like Cara who struggles with seeing a way out of this mess and who literally lives paycheck to paycheck and often overdrafts her account, the idea of having thousands of dollars to spend as she pleases every month is a HUGE motivator.

But again… That’s a great big picture to visualize, but it’s the incentivized savings that will get her there, not just the visualizing.

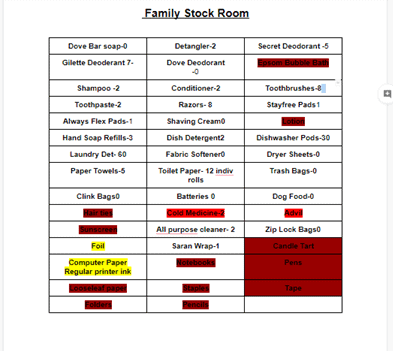

Why you need a stockroom.

One of the categories we have is a stockroom. The reason why we do this is because having a stockroom is an easy way to control your spending. Ever walk into Walmart or Target for one thing (like deodorant) and leave with $100 worth of stuff you didn’t realize you needed?

Every time you “run” into a store is a roll of the dice that you’re going to blow the budget. We create stockrooms because that eliminates those errands and lets us predict the cost of what we need to run our home and our lives.

This is Cara’s stockroom list…

She had a lot of things on her list that were “wants” and not actually needs.

The only items that go on your stockroom list are items you would actually run out and buy today if you ran out.

If you run out of Febreze plugins, you’re not running out to buy new ones, so those don’t go on the list. If you run out of deodorant, you’re running out today to get that, so that does go on the list.

We removed things like notebooks, paper, and pens from the list because they don’t meet the qualifications that she’d run out to replace them (and she admitted that she had dozens of each around the house).

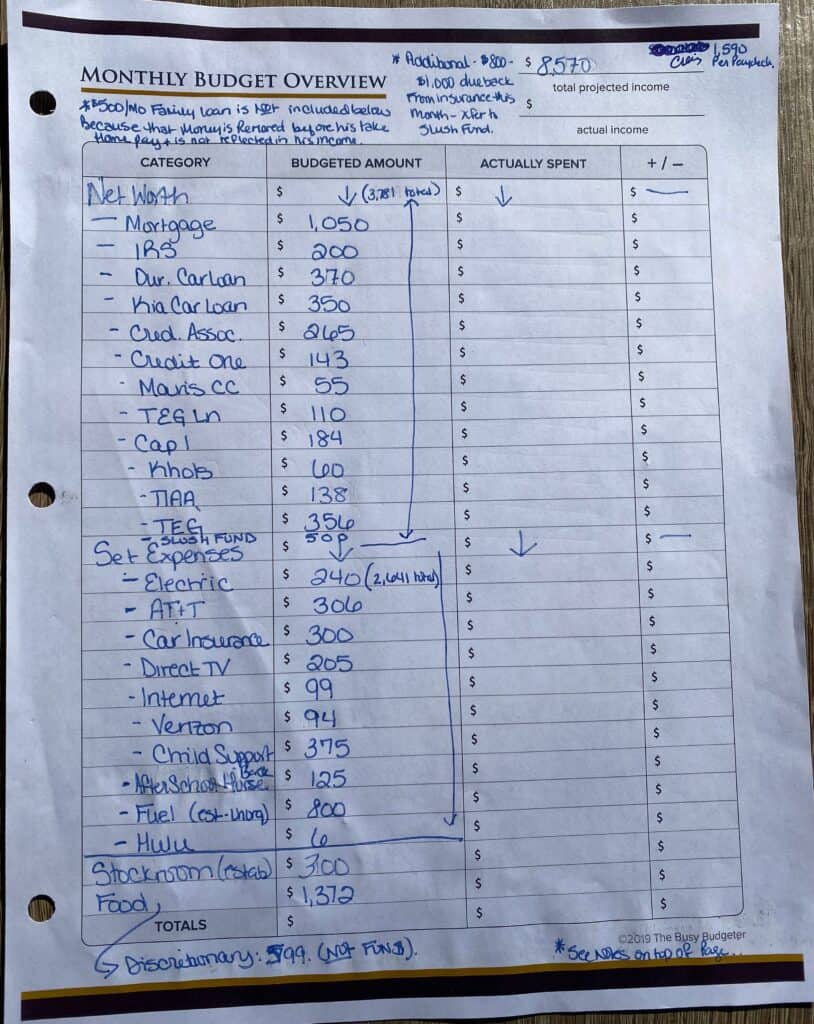

Step 12: The monthly budget overview.

Monthly sheet to track each debt owed, amount budgeted and amount actually spent.

Now that we know what we’ve been spending and we know exactly what our situation is (admittedly not good), we can make a plan for the future.

Why? The Monthly Budget Overview is what people typically consider to be the budget. It tells your money where to go this month.

For income, Cara added her and her husband’s income for this month. Since there were 5 weeks in the month instead of 4, and her husband gets paid every other week, he gets 3 paychecks.

The difference between what we did now and what you’ve done in the past is that this time we know what’s realistic and what’s not.

For example, dropping your grocery spending by 60% is not realistic. You should never set a grocery budget less than 20% lower than what you spent last month.

You can still reduce it lower than that (especially when you use this trick…)

But trying to budget groceries for less than 20% of what you spent last month is guaranteeing that you’ll fail.

And we have a plan (incentivized savings) to retrain your brain to stick with it so you don’t have to rely on willpower (which also isn’t going to happen.)

- We’ll do the monthly budget by categorizing each item into one of the 5 simple budget categories. We have all of our debt under net worth (remember, we actually want to overspend in net worth! That’s a good thing if we go over there.)

Cara added $500 to her emergency fund (she calls it a slush fund) which currently has zero in it.

This is to give her a buffer in an actual emergency so she never has to use her credit cards (or take out another loan) again. Right now she’s in a vicious debt cycle. Anything that happens out of the ordinary will cause her to get more debt.

Ironically, having the emergency fund means that her worst case scenario is just using that money, and that gives her brain time to think outside the box.

- Without an emergency fund, you think, “I’m screwed anyway.” I’ll just get a loan, or put it on a credit card, etc.

- With an emergency fund, you think “I’ve got this” and you find another way.

Step 13: Determine set expenses.

- Under set expenses, we list monthly bills that aren’t debt like internet, electric, etc. Usually, set expenses are things that don’t change. They’ll cost the same month after month with little variation and you can’t really choose to spend more.

There’s two exceptions to this:

- You can also put fuel under this category using your highest normal fuel spending for the month and depending on your situation, you can also put medical expenses here…

- You should put medical expenses here if you have fairly predictable medical planning. Meaning, you spend $100 on medications every month, you’re 13-year old has therapy once a week for $65 and you guys rarely go to the doctor but when you do, your insurance pays for it and you’re billed your copays after the fact.

Then just go ahead and add the $165 here. When you get the bill for the copays, you’d also add those under set expenses and plan for them that month.

If you have a more complicated medical situation, (like if you have a health share and often have to self pay out of pocket, while waiting for reimbursements or you have a medical condition that requires frequent doctors visits at a high cost) then you need to set up a separate medical fund.

Additional bank accounts.

You can do this by starting an additional bank account with its own debit cards and checks. Just set up a transfer every month with a specific amount of money for the medical fund. List your medical expenses here. Let’s say $215, and that $215 would get transferred to the medical fund account. You should try to add an additional $50 a month, which would start building up until you needed it.

For Fuel, Cara has no idea how much she spends on fuel, because she lives in a remote area without grocery stores, so a lot of her groceries were purchased at gas stations. She has no way to know whether the $30 gas station purchases were fuel or groceries.

That’s fine. We’ll figure that out as we go. We used a high estimate of $800 a month for fuel for her family (remember, they live in the middle of nowhere and they have 4 teenagers).

As we get more detailed feedback this month, we’ll be able to adjust that accordingly for next month.

Step 14: Create your stockroom list.

We went through Cara’s Stockroom List and gathered up the supplies she had and stuck them in a corner. Then we made a Walmart grocery list using the Grocery Pick Up app of what she would need to have a fully stocked stockroom for 4 months.

Hint: We don’t stock food. Some people save money when stocking food, some people spend more (because food expires) so, it’s not a universal best practice. We consider it to be an advanced move and ask you to not stock food unless you are already doing it successfully.

Don’t over-complicate this.

- If you’re in a financial bind and think you can’t do this, go to the dollar store and buy shampoo, deodorant, soap, toothpaste, toothbrushes, trash bags, hand soap, paper towels, toilet paper, etc. Many readers have been able to do a bare-bones list in their budget binder for $20.

Fun fact: Because I know the universal cost savings of a stockroom for everyone, finding a bare minimum stockroom is the only purchase I’ll ever encourage you to make with a credit card.

I don’t mean the cost savings of buying shampoo for $1 at Walmart versus $2.15 at the grocery store. I mean the cost savings of the extra $30-$100 of impulse purchases every time you walk into a store.

Not to mention the gas and the potential of hitting the Chick-fil-A for dinner instead of eating at home because you’re driving past it.

This has been A/B tested over and over and this will make a massive difference in your life.

Should I use a credit card.

I don’t think credit cards are evil (the financial world is full of people with willpower that travel for free using them. But we are not those people. We are the people who pay for the organized people to travel for free when we use them.

For food: We attempted to reduce Cara’s spending to the national high level for her family size. I’m usually not a fan of trying to reduce your grocery spending by more than 20% a month. It’s a bit of psychology, but I find the higher allowed limits actually lead to less spending. While more restrictive limits actually lead to blowing your budget.

In this case, Cara really felt strongly that they could do with it, so we went with it.

One of the problems in Cara’s case is that they were living so far above their means every month that it would be difficult to reduce her spending in smaller percentages (like 20%) and not need to get new debt to cover the overages.

Where to find extra money.

One of the ways you can circumvent that is to say “I know I’m going to spend this amount.” “Because I’ve spent this amount every month. So now my goal is to find enough or make enough extra money this month to have that amount available without debt.”

The easiest way to do that is to start decluttering your house. Sell things on Facebook Marketplace and gather that cash. If you’re a mom at home, you can also offer to watch kids on weekends or plan PNO (parent night out) for kids to come have a movie and dinner at your house while the parents go out to a date night.

You can also flip jeans from thrift stores and sell them on eBay or Poshmark, do User Testing, walk dogs, log some hours doing Shipt shopping, or any other of a million things to make quick cash.

And if you don’t end up needing it? Great. That’s extra money to go towards your goals. Aren’t you crushing it? Look at you go!

Step 15: Planning the discretionary category.

This is NOT FUN MONEY or blow money. When you look at the discretionary category, you think to yourself “I want new shoes. I can buy them and put them under discretionary.”

Nope. That’s not how that works.

Think of discretionary as a mini emergency fund just for the month.

Hint: We don’t talk about fun money a lot in this article, because in this situation we aren’t in a position to be assigned fun money. Unless it’s earned blow money by coming in under budget.

As you make progress, fun money can become it’s own category and you get an assigned amount of money every month to spend as you want.

You shouldn’t be buying fun things from this category. That would go under fun money.

Discretionary is for things that came up unexpectedly. The fridge broke, you need a babysitter for an unexpected work meeting, you forgot about a kid’s birthday (don’t judge). It’s not for new iPhones or anything like that.

Our goal is to prepare for and plan expenses.

Like, if you know the kids need new jeans for fall.

Your monthly budget would say for discretionary…

$100 kids fall jeans

$499 other discretionary.

So you can plan some discretionary and leave overflow as well.

- Your goal is to get through the month spending as little discretionary money as possible. Then you get to have 20% of it to blow on whatever you want guilt-free.

Discretionary money.

If you approach discretionary money as “this is money I’m allowed to spend”, it will be gone by the third of the month, and you’re going back to the credit cards.

What if you fail? What if you end up spending every cent of that discretionary money on stupid things? Awesome. You still win. Because last month Cara spent $2,834 on discretionary.

Anything better than that is “winning”. Even if she completely screws this up.

Winning means doing better than last month. And next month will be better than this month.

THAT’s why it’s important that you look at where you’re starting now when you start the budget binder.

If you don’t do that… it’s like giving up the diet because you didn’t lose 50 pounds in a month. 🙄

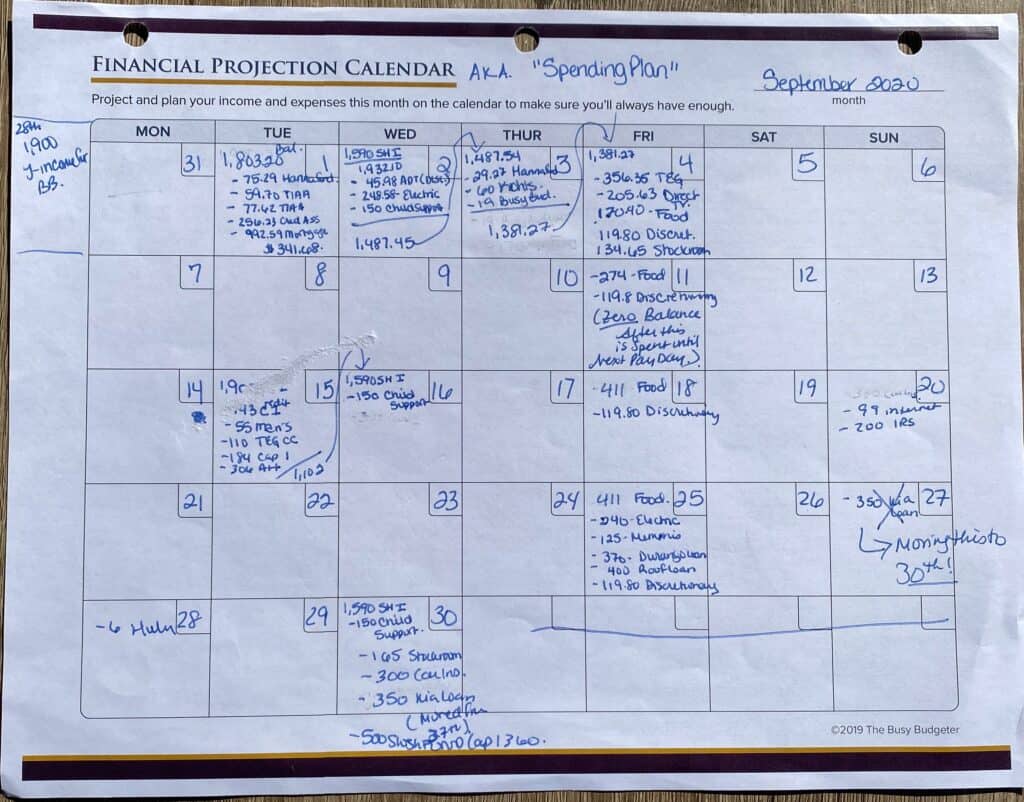

Step 16: Complete the financial projection calendar.

Financial projection calendar worksheet to track upcoming purchases so you can plan ahead.

Why a monthly budget is so important is because it gives every dollar coming in a job, or something to do. But, it’s worthless unless you know when money is coming in and when money is going out. Usually, when people start doing this budget binder, they see there are some issues that need to be adjusted.

Like in Cara’s case, they make enough money over the month to afford that budget we set out. But, because one of those checks is coming the day before the last of the month, she doesn’t have enough to give herself a weekly grocery allotment without overdrawing her bank account.

One of the reasons why we use the Financial Projection Calendar in our budget binder is that we can make changes to accommodate for that. We can permanently change the due date of certain bills by calling (most places will let you adjust due dates permanently), and we can make an arrangement to pay something late. Or, we can focus on coming up with extra cash early, or having a spending freeze to get through a tight week.

The point is that if you know it’s coming, there are dozens of ways you can prepare. But, if you just set a monthly budget and assume it will all work out, you’ll overdraw your account. Or, you’ll switch to a credit card because you’re not prepared.

Here’s an example.

In Cara’s case, we set the dates in her budget binder that money comes in and comes out for the whole month. She updates this every morning (it takes less than 2 minutes and fits in beautifully with your normal schedule routine if you’re in Hot Mess to Home Success which she is) with any spending from yesterday.

Some people like to track their spending right on the Financial Projection Calendar and some people like to do it on the Scratch Pad.

- I recommend using the Scratch Pad and leaving the Financial Projection Calendar as a distribution plan (when money comes in and is released to spend).

What we’re looking for when we do the spending plan is weeks when we need to have money for groceries and fuel, but it’s not there.

- To make it more likely that we’ll stick to the budget, we distribute monthly money for discretionary and food on a weekly basis (or by paycheck, whichever you prefer). Keep in mind though, because when the money is coming in, every week for this first month, may not be the same.

Be creative.

Cara wasn’t in good standing with most of her creditors so she didn’t feel comfortable changing her due dates. But, she was super motivated, so she chose to have a spending freeze the week we set up her budget. They would eat through everything in her freezer and pantry, leaving just a bit of money for milk and produce and then do a 15-minute meal plan next week.

The goal is to make an extra $200 by the 11th, to make sure that her account doesn’t dip to $0 (where it’s projected to) to give her a little buffer. She’s going to do that by selling an RV they own (making much more than $200, but putting the rest towards debt except for the $200).

She’s also buying her stockroom items in waves so she doesn’t go over what she’s capable of spending in a week (since one of her paychecks are coming in just before the end of the month).

Planning for the week or paycheck.

It sounds silly but after you do your monthly budget in the budget binder, you also need to budget for either the week or the paycheck.

Because again, even if your family will make $8,000 this month, you won’t necessarily have that $8,000 at the beginning of the month (most people don’t). You’ll get it in pieces as your paychecks come in.

- So, you can use the Easy Weekly Budget Sheet in the budget binder to plan what you’ll spend either every week or every paycheck that still fits into your monthly budget. Your monthly budget is the bigger picture plan and the weekly or paycheck budget is the action plan.

Hint: Some people choose to skip this sheet in the budget binder and just sort out the dates that their money is going in and out in the Financial Planner Calendar. That’s fine too.

This sheet is incredibly helpful though for people who are new to budgeting, so if you’re just starting or have tried and failed to stick to a budget in the past, use this sheet for at least 3 months until you’ve established the habit and can decide for yourself if you really need it without risking falling off the wagon.

To use this sheet…

-

- Determine your weekly or paycheck income and write that in.

- Set a budget for each category (making sure it aligns with your monthly budget).

- Track your daily spending: This is also one of the places that you can track your daily spending, and it’s where I track mine now. To do that, I’d suggest using a pencil or Frixion pens so you can write in planned expenses and then erase and adjust them as they change.

- Total your spending at the end of the week.

- Figure out the total amounts that you went over or under budget. How much did you overspend? How much did you underspend? Add those numbers to the +/- boxes for each category and mark down if you were over or under.

- Calculate 20% of the total amount in each category you were under budget. Here’s how you do that. If I was under budget by $100 x .20 (20 percent) = $20. $20 goes into my blow money account.

- Add the remaining money (the other 80%) to the extra debt payment section for each category. Hint: When you’re first starting out, you should pay this extra debt payment right away. Until you have a good grasp of budgeting, you don’t want “extra” money lying around because you’ll ALWAYS find something that you need it for.

Cash versus debit (pro/cons).

People often say that cash is king. It was made popular by financial guru Dave Ramsey and while we’ve used cash only for months at a time, I also feel like it’s not a sustainable life choice for someone who is naturally a bit of a hot mess.

The idea behind this is that by using cash, you “feel” the loss of the money as you spend it. It makes you super conscientious of the money that you waste. And it works really well to reset the way your brain thinks about money (similar to the way that a spending freeze works).

When you have to empty your wallet to buy something for $200, it feels a whole lot more serious than just swiping a card.

What if cash doesn’t work for me.

That being said, I’ve also seen moms in the grocery store with two crying kids trying to pay cash and put change back into the envelopes while logging purchases. If you’re dedicated enough to stick with it, log appropriately and keep your envelopes sorted (and safe), it can be awesome.

But if you don’t… Then you have no idea what you spent or where and it’s one more thing you have to keep track of.

Plus, it makes automation hard. Automation changed my entire life. Part of automation is replacing errands with online options. Like getting Amazon to deliver the birthday present you’ll need this weekend or getting Walmart to deliver your groceries to your door.

Shopping online.

But when you shop online, you can’t pay cash. So you lose the convenience (and the equivalent of 8 hours a week) of being able to shop online frequently.

That’s not even counting the issues that cropped up in 2020. Suddenly, a ton of businesses were not accepting cash.

Am I anti-cash? No way, I think if you want to try it, it’s worth the try. And, you’d have a huge boost to your financial mindset.

But if you struggle with it, or don’t want to, the way we budget…

- Will work just as well

- Require less effort

- Allow you to track every purchase

- Let you shop online

Using credit cards.

While we’re on that topic… I get asked about credit cards a lot.

It’s not that I think credit cards are evil, but I don’t recommend them.

I know tons of financially savvy people with strong willpower who travel for free with credit cards every single year. They pay off their balance monthly and it works for them.

I am NOT one of these people.

If you’ve read this far, you are likely not one of those people, either.

In fact, you and I are the people that pay a ton of interest for our stupid impulse purchases. We make it possible for my financially savvy friends with willpower to travel to Hawaii every year.

If you’ve been using credit cards and paying them off every month… Then I don’t think you’re stupid for using one.

But the vast majority of our readers won’t do that. It’s almost impossible to break out of this cycle while still using credit cards in any capacity. So, I skip them and also think you should skip them.

Step 17: Set up fun accounts and emergency funds.

Multiple bank accounts are one of the best assets you can have if you struggle with sticking to your budget.

Ally Bank is my favorite bank for blow money (in case it matters, you also earn a pretty decent interest rate on money markets here, like 1-2% depending on the market rates) but you’re a rare bird if you can keep money in your blow money account.

- Open one account for each of you (you and your spouse/significant other) for blow money.

- Request a debit card for this account and use an online bank (that has free ATM access and no fees, minimum balances, etc).

My blow money immediately goes to Thrive Causemetics, Amazon, or the Hearth and Hand line at Target. You can request a checkbook for this account too (like starter checks) if you think you may need them but, it’s not really necessary.

Once you have them set up…

- Set up transfer to this bank from your main checking account (this usually takes 3-5 days to complete). So when you earn blow money you can transfer it to your blow money account.

Hint: It’s going to take 1-3 days to transfer. So it’s important that you don’t allow yourself to spend your blow money. It can only be spent AFTER it lands safely in your blow money account.

Making the system work for you.

- Then, in addition to your main checking account (the one that you’ve always used), I want you to create one more checking account at the same bank and order checks for it, no debit card.

This is your check holding account. Every time you write a check (whether it be to pay a bill or money that is “ear marked” in your account that you can’t actually spend. I want you to transfer the money to this account first and then write and send the check from this account. This is the only account you can write a check from.

This means you never have to worry about writing a bad check. And, except for your auto pays (like things that are automatically removed from your checking account), you’ll always know your bank balance is your bank balance.

You won’t have to wonder how much of that is already ear marked for checks, etc.

Hint: Until you’re really good at budgeting (like years into this) don’t use auto pay. Pay your bills every month using checks and transferring the money to the check hold account.

For the things that need a subscription (like Netflix, Hulu, Amazon Prime, etc.), you could have another bank account. One that’s set up for any “autopay” and that you transfer money into monthly or by paycheck.

Step 18: Calculate your blow money.

- Blow money is a 20% cut of the money you save every month. So, if your weekly grocery budget is $200 and you spend $100 – then you take $20 and transfer it to your blow money account. Then take the $80 leftover and apply it to your debt.

- Incentive money (blow money and the extra debt payment) is paid out weekly during your weekly budget meeting.

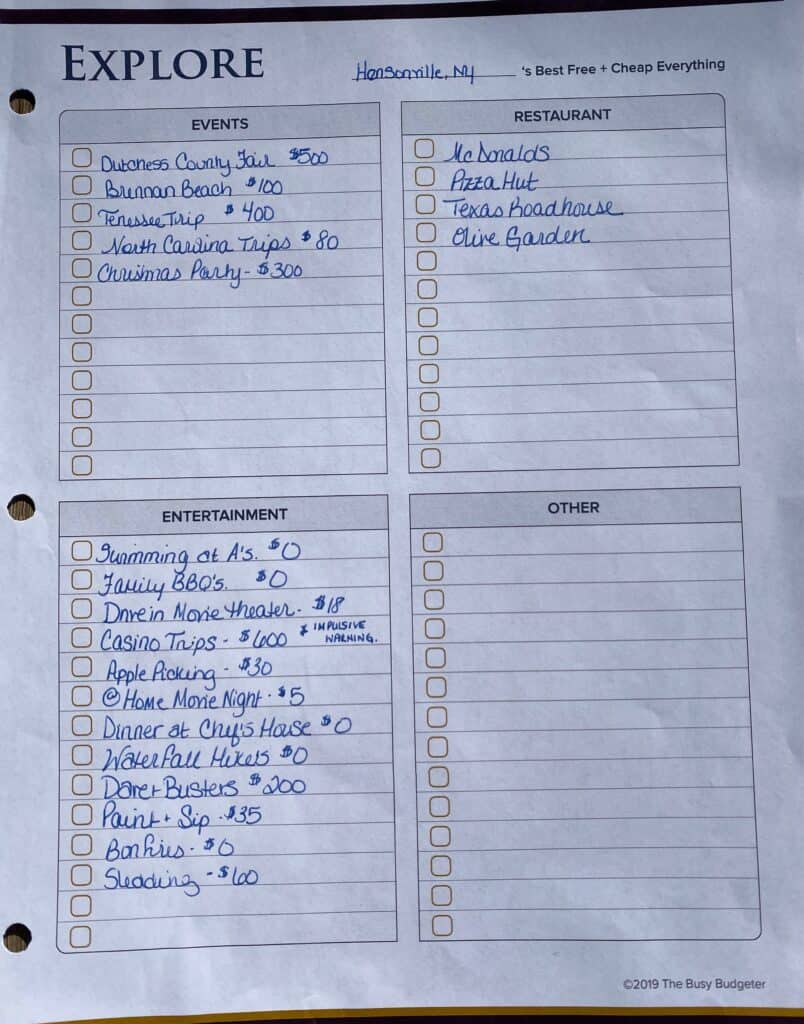

Local deals and entertainment.

One of the ways you can make a big impact and reduce your spending is to have well thought out options for entertainment. Do some exploring. Look at local options of best restaurant deals, events you love, and the things you love to do.

- Then write down an estimated cost of what those things will cost you.

On days where your budget is tight and you need to spend less, you’ll have a list of fun things that you can do…

- With the kids.

- For a date night.

- With friends that are free.

The days that you have a little extra blow money or you want to budget for something special, you know the cost of those things ahead of time. This way you can plan for them (or accept the fact that you just can’t afford it right now).

What surprised me about doing this is how many things I love doing that cost zero dollars. And, how infrequently I thought of them until I put them on a list. I just create a list and stick a copy in my budget binder.

Think outside the box.

Also, packing picnics to places was huge. Because I could fit that money into our food budget without needing to budget for extra.

Cara just started so this isn’t the best example.

But, If you look around town at special deals, a lot of places run really great deals… kids eat free nights, or taco Tuesdays, etc. I write those down so when we plan to eat out we can take advantage of those.

We have an epic Mexican joint locally that has $1 tacos on Tuesdays and free chips and salsa. Every, we meet friends there Tuesday and all 9 of us eat for about $20.

There’s also a BBQ joint that has $1 pork sliders and $3 fry baskets.

Find the best deals.

You can help yourself find the best deals by asking in a local Facebook groups. Find what restaurants have awesome deals locally. Write everything on the list. And, write down what your bill ends up being at your favorite restaurants.

This way if you need to eat out, you can choose something that fits the budget.

Hint: Another favorite example of mine is to pack apples and water from home for nights we have soccer and then just buy a 30 count chicken nugget from Chick-fil-A for the kids to share. Your example of this may include chips and soda or whatever you’re into. But the idea is the same.

Step 19: Track spending weekly.

Scratch worksheet to keep track of things that you purchase.

- Track spending on the scratch pad every day. I do it in my budget binder when I eat breakfast at the kitchen counter every morning.

- Pull up your bank statement for your main checking account on your phone, and just log in any purchases you made in the scratch pad categorizing them into one of the 5 simple budget categories.

- At the end of the week (and then again at the end of the month) add up the totals of spending and put it in the Spending Tracker.

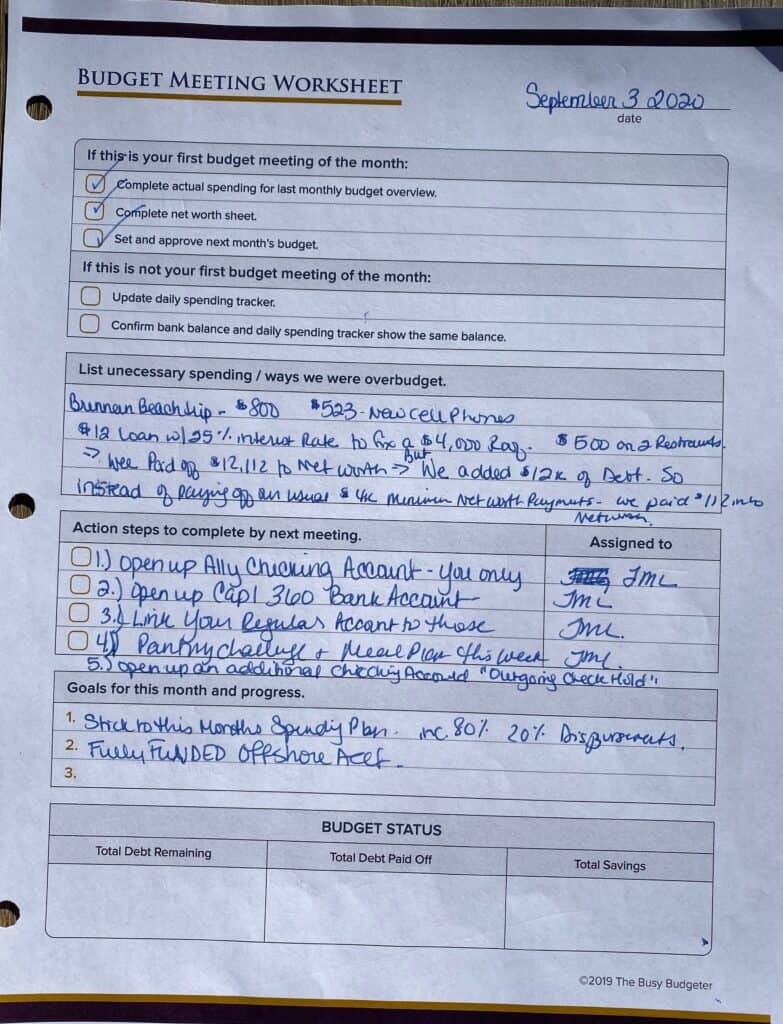

Step 20: Schedule budget meetings.

Budget Meeting worksheet to update and track weekly budget progress and assign goals and tasks.

Start having budget meetings, and do this monthly…

- Once a week on a schedule, have a budget meeting. These can be quick and easy.

- A few minutes at the start of dinner on Fridays.

- Via phone calls (if you have opposite schedules)

- On a date night if you have the time and want to make it special.

Hint: make it the same day every week. It just makes it easier to remember and to set a schedule. Write it in your calendar so you get a visual prompt (especially in the beginning).

Our Budget Meeting Sheet has all of the instructions written out for you so you remember what you need to do.

But you’re basically…

-

- Checking in

- Talking about what you did right

- What you did wrong

- How to make it better or easier next week.

- Then assign yourself between 1-4 action goals. And complete them before the next meeting.

- You can track your goals at the bottom. I suggest sticking to shorter goals here so you can see faster progress and stay motivated. Goals like “pay off capital one card with a balance of $5,600,” instead of “become debt free,” will work better.

Step 21: Budget maintenance.

We like to teach bare minimum effort on a consistent basis. Once you’ve set this up, you follow a quick and easy maintenance plan. It’s the bare minimum effort you need to do on a consistent basis to stick to your budget.

- It’s about 2 minutes a day to update the budget binder.

- 15-30 minutes weekly to do the budget meeting.

- And 5-10 minutes a month to set up the next month’s budget.

The rewards are built into the system so that you actually want to do the bare minimum effort (because relying on your willpower is not going to happen).

When you get “paid” blow money to show up to a budget meeting… suddenly, you start to love budget meetings. 🙂

Daily Action Steps.

Once the Easy Budget Binder is set up, it will take you 2 minutes a day to maintain it.

- Stick the budget binder on your kitchen counter or somewhere that you sit frequently.

- Add your spending to the scratch pad every morning. You can get your spending straight from your banking app.

Weekly Action Steps.

- Calculate last week’s spending (just add up the numbers). It should take about 5 minutes.

- Have a budget meeting. (This will take about 5-20 minutes and can be discussed over dinner, in bed, or as it’s own little date night ritual.

- Distribute “blow money” and extra payments to debt based on your spending.

- Set up the next week’s spending plan (if you do your spending plan weekly). Takes about 5 minutes.

Monthly Action Steps.

- Fill out next month’s Budget Overview. This should take about 5-10 minutes.

Warning: What to do if this doesn’t work:

We specialize in helping the most severe cases of chronically disorganized people completely transform their budget and their home while working with their unique personality (instead of the one they wish they had).

And we’re really, really good at doing it.

We’ve helped hundreds of thousands of people get their budget under control. The trick is a budget binder and a system that works. I’ve been featured on Forbes, Entrepreneur, Country Living, Fox Business, and Motley Fool in the last 7 years. That’s how long we’ve been teaching this.

Many of you will implement this budget binder and find it’s incredibly easy. You also might find it will be the key you’ve been missing all along. You’ll be able to stick to the budget no problem. Within a few months to a year, you won’t even remember that you weren’t naturally awesome at budgeting.

But a few of you will fail at this budget binder too. You might get overwhelmed setting it up. Or, you’ll set it up but forget to maintain it. Or, you’ll go right back to what you’ve always done. Your goal is always to do better than yesterday.

Avoid overwhelm.

Using a budget binder will help, but it’s not your fault if you end up “falling off the wagon”. This means that you’re likely one of our severe cases (and I promise you, we’ve helped worse).

It just means that we need to quickly teach you the foundational habits that support your ability to save money.

I teach you how to work with your personality to get the dishes, laundry and your schedule book (planner) done every day.

I know you’re probably thinking, “what does that have to do with budgeting?”

Those 3 things have a MASSIVE impact on your ability to budget and for the most severe cases we need to teach you our system of bare minimum consistent effort to get those things done while working with your unique personality.

When we teach you how to do those simple skills our way, it removes any barriers to sticking to your budget.

Simple skills that work for your life.

Because it teaches you how to plan your day in a way that works for you. The dishes are always done making it easier to find the motivation to cook at home (or just accept your busy schedule and budget to eat out).

You’ll have more time to yourself, your home will run itself, and you’ll have less stress. All of that will put you in a position where you can try this again. And finally, have it work the second time.

If you’re one of the severe cases, we specialize in this. The best way to get this done is by joining the step by step complete course Hot Mess to Home Success. The course will teach you our proven system of bare minimum effort on a consistent basis. It will completely transform your home, budget and life.

Hot Mess to Home Success is not always open but when you join the waiting list, you get the starter program Trashed to Total Home Transformation for free.

Grab the Trashed to Total Home Transformation Starter Program for Free by joining the Hot Mess to Home Success waiting list here … you can get that done in just a few days and then the Easy Budget Binder will work for you too.

Guaranteed. 🙂

Ready to start? You can get your copy of the Easy Budget Binder right here.

I bought the budget binder but can’t find the easy weekly budget sheet… Where can I find it?

Hey Sandra! Email is at [email protected] and we’ll get you squared away.